There is a fundamental change in the insurance industry. The expectations of customers have changed, the regulatory environment has become increasingly complex, and the competitive environment has never been as challenging. In the case of executives of insurance organizations in 2026, the need to modernize is no longer something in the future but a current operational requirement. The key to all this change is a vital choice: how do we select, develop, and implement the appropriate insurance software tools that support your business strategy, technical landscape, and long-term business growth goals?

The guide is addressed to C-suite executives, CTOs, and top technology decision-makers who require a strategic and coherent guide to assessing the current insurance software development investments. Do you want to be a legacy carrier and modernize, or an up-and-coming MGA looking to gain market share faster, or a specialty insurer seeking to differentiate yourself competitively? The choice you make today concerning software will determine what your competitive position will be over the next decade.

Why Legacy Systems Are No Longer a Safe Option

Over the decades, the insurance carriers worked on platforms that were not developed with technology in place when the business needs were not as complex, the customer demands were less, and the market change was not as fast. Such systems were constructed to be durable, and in most instances, they are, well beyond the usefulness of their service.

The maintenance of legacy infrastructure is becoming very expensive. Some of the major pain points are:

- Increased maintenance expenses: IT teams use most of their time and budgets to maintain the old systems instead of constructing new functionalities.

- Failure of integration: It is more complex and costly to integrate with modern sources of data, digital distribution channels, and third-party APIs.

- Competitive disadvantage: Insurtech startups and digitally native MGAs are introducing products and serving customers faster and more efficiently than the legacy-bound carriers can.

- Regulatory risk: The systems are outdated, which introduces increasing compliance risk as data privacy, consumer protection, and financial reporting requirements increase.

- Manual process dependency: The dependency on manual processes will make auditing risky and may result in fines for non-compliance.

The modern insurance software solutions address these issues directly. They make compliance cheaper and simpler, speed up product development lifecycles, facilitate online interactions with customers, and offer the analytical basis that data-driven decision-making needs. Executives are not asking whether to invest in modernization but how to strategize on that investment.

The global insurtech market size is evaluated at USD 50.03 billion in 2026 and is anticipated to attain nearly USD 739.69 billion by 2035, with a strong CAGR of 35.27% from 2026 to 2035. The rise in fraud detection and high investment in traditional insurance firms drives market growth.

Custom Insurance Software Development vs. Off-the-Shelf Platforms

Among the most significant choices any insurance executive will encounter in a modernization project is the choice to develop their own insurance software or acquire an existing off-the-shelf solution. Each of these options has valid merits, and which option is the correct one largely depends on the business model, competitive strategy, and technical context of your organization.

Read More: Pricing Models for Software Services – Fixed vs. Hourly Rates Explained

The Strategic Case of Custom Development

Developers design tailor-made insurance software to meet your specific business needs. It does not depend on a vendor’s product roadmap, licensing model, or assumptions about how insurance companies should operate. In the case of carriers that offer differentiated products, have specialized underwriting requirements or complicated distribution models, such a degree of control is a strategic requirement. The main benefits of the development of custom insurance software are:

- Full product logic: Free control over rating algorithms, coverage structures, and underwriting rules without platform limitations.

- Higher integration performance: Custom APIs and middleware tailored to your environment will provide more reliable, higher-performance connectivity than platform adapters.

- Long-term flexibility: Systems scale along with your business without relying on vendor roadmaps or licensing limits.

- Competitive differentiation: Proprietary capabilities not replicable by competitors on commercial platforms.

- Ownership and control: You own the system; that is, you determine its further course and priorities of development.

Take into account the underwriting and rating role. Off-the-shelf platforms provide configurable rating engines, although there are constraints in configuration. When your competitive edge lies in proprietary risk assessment models, actuarial algorithms, or data-driven underwriting standards specific to your business, an abstract platform will ultimately limit you in what you can do. The development of custom insurance software eliminates those restrictions.

When Off-the-Shelf Platforms Make More Sense

The market of commercial insurance platforms has become mature. Contemporary solutions provide a truly strong capability. These platforms have strong benefits to many organizations, especially those in new markets or rolling out new product lines at a very rapid pace:

- Faster time to market: Achieve production in a fraction of the time it takes to build off-the-shelf.

- Lower initial expenditure: Subscription fees or licensing fees spread the costs more uniformly and predictably.

- Time-tested technology: Battle-tested platforms lower the risk of implementation of core policy administration functions.

- In-built controls: Most new platforms have regulatory-compliance controls by default.

- Rich partner ecosystems: Pre-built integrations with common third-party data providers and distribution channels

The platform method usually yields a higher short-term payoff on investment in the case of emerging carriers and MGAs with limited capital bases. The objective is to access the market, validate the business model, and earn revenue, not to create technology in and of itself.

The Hybrid Approach: The Best of Both Worlds

In practice, most of the most effective insurance technology deployments are a combination of the two methods. A carrier may adopt a proven commercial platform to administer core policies and invest in custom insurance software to do what really sets their business apart:

- A specialty line’s proprietary underwriting workbench

- An agent portal that is modeled around your distribution model

- An individual customer-facing mobile application that differentiates your brand

- State-of-the-art claims analytics applications developed on your proprietary data sets

- Personalized reporting and control boards in line with your regulatory requirements

This hybrid model enables the organization to act swiftly in terms of commodity capabilities and competitive differentiation where it is most needed.

Read More: How to Hire a Software Development Team

Understanding the Insurance Software Design Imperative

Insurance software design principles cannot be isolated from technology decisions in insurance. The architecture choices taken during the early phase of a software project have a long-lasting impact on the system. Bad design decisions produce a technical debt that makes subsequent development slow, maintenance more expensive, and eventually constrains the business value the system can provide.

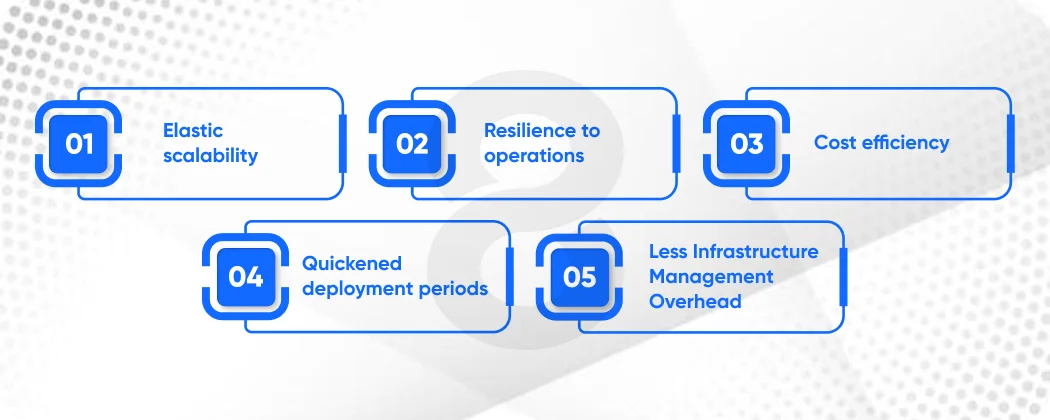

Cloud-Native Architecture

The current insurance software design is cloud-based, starting with its principles. Its main advantages are the following:

- Elastic scalability: manage peak workloads during open enrollment, catastrophe claims spikes, or end-of-quarter reporting without overprovisioned infrastructure.

- Resilience to operations: Cloud-native applications based on microservices and containerization do not introduce single points of failure.

- Cost efficiency: Only pay for compute resources on demand instead of having fixed on-premises infrastructure.

- Quickened deployment periods: Containerized services can be modified and deployed separately, enhancing the rate of innovative processes.

- Less Infrastructure Management Overhead: Managed cloud services remove the operational overhead of maintaining servers, databases, and networking infrastructure.

API-First Integration Design

Successful insurance software development considers APIs as a main architectural delivery, rather than an add-on. Properly designed APIs allow easy connectivity to:

- Third-party data providers, such as credit, motor vehicle, and property data providers

- Aggregator platforms and digital distribution partners

- Bordereaux reporting systems and reinsurance systems

- New sources of technology include telematics, IoT, and satellite images

- Compliance platforms and regulatory reporting systems

The most important aspect of insurance API design is security. There should be ways to authenticate the identity of calling systems with certainty. Access control policies should be that each integrated system has access to only the data it has permission to view. Extensive API activity logging facilitates troubleshooting, as well as monitoring regulatory compliance.

Security by Design

Insurance systems deal with some of the most delicate personal and financial information ever to exist. The design of the insurance software should consider security as an architectural requirement and not a feature that is introduced once the core system has been established.

The key security principles are:

- Threat modeling throughout the architecture process

- Security-related code reviews that are performed during the development lifecycle

- Penetration testing is done prior to any system entering production

- Zero-Trust network architecture, whereby there is no default trust on any system or user

- Multi-factor authentication of all user and system entry points

- Data-in-transit and data-at-rest end-to-end encryption

- Detailed audit trails to support regulatory compliance and explainability of AI

Read More: What Is QA Testing in Software – Our Experts’ Insights

Navigating Legacy System Integration

For established carriers, the most technologically demanding aspect of any modernization program is integrating new insurance software with existing core systems. Years of investment in technology can not just be swept away.

The Strangler Fig Pattern

The mode of migration of the strangler fig has become the standard mode of dealing with this challenge in the industry. It is done in a well-defined process:

- Determine discrete capabilities: Identify discrete business capabilities that can be extracted from monolithic legacy systems

- Develop new microservices: Re-architecture every capability into a cloud-native service

- Integrate concurrently: Tie new services to both the old systems and other new features

- Validate and cut over: Test every migration step separately before retiring the legacy function

- Repeat step by step: Repeat the process capability step by step till it is totally migrated

This will be a very risk-averse way. The steps are scoped, tested, and validated separately. Those organizations that have managed to implement this approach successfully report:

- Reduction of operation costs by 25-40 percent

- Improvements in claims processing up to 60 percent

- Considerable human error minimization in core insurance processes

- Greater agility to respond to regulatory and market changes

Data Migration and Continuity

Migration of data is always underestimated as a complex and risky issue. Key considerations include the following:

- Data quality assessment: Audit legacy data as complete, consistent, and accurate before migration.

- Mapping and transformation: Design explicit rules of how old data structures can be converted to new data models.

- Regulatory defensibility: Make sure that migrated information is in line with existing compliance and audit provisions.

- Testing at scale: Before full production is cutover, test the accuracy of migration on representative samples.

- Rollback planning: Retain the right to restore the old source data in case of serious problems that arise after the migration.

The executives need to realistically budget data migration as one of the workstreams in any modernization program. One of the reasons why insurance technology projects are over-budgeted and over-scheduled is the failure to do so.

The insurtech (insurance technology) market size is expected to see exponential growth in the next few years. It will grow to $128.12 billion in 2030 at a compound annual growth rate (CAGR) of 38%.

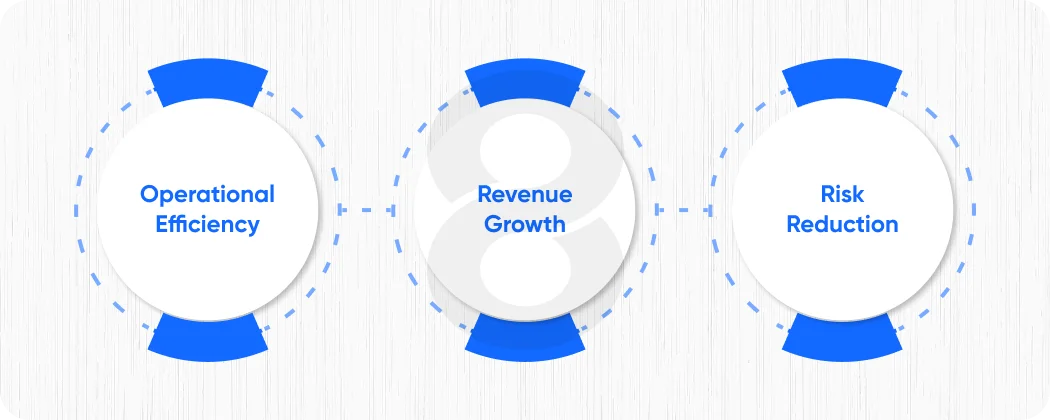

Building the Business Case: ROI and Time-to-Market

All the insurance technology investments should have a clear business case. Contemporary insurance software systems provide their returns in three main avenues:

1. Operational Efficiency

- Policy administration automation saves on labor expenses.

- Automated claims help to remove bottlenecks and cycle times.

- Automated compliance reporting saves on preparation time and the cost of audits.

- Less human error minimizes downstream correction and rework costs.

2. Revenue Growth

- Quicker product launches allow responsiveness to market opportunities to be quicker.

- Digital distribution channels increase the market reach without a commensurate increase in cost.

- Excellent customer and agent experiences lead to increased retention.

- The sales and servicing process are less frictional with self-service capabilities.

3. Risk Reduction

- The contemporary compliance systems decrease exposure to regulatory violations.

- High-level analytics enhances loss ratio and fraud detection.

- Improved data quality facilitates more precise reserving and financial reporting.

- Strong audit trails minimize vulnerability to regulatory inspections and lawsuits.

The realistic time lines consider variations depending on scope and complexity:

- Special-purpose applications (agent portal, claims intake, customer self-service): 3-6 months agile approach

- Mid-scope implementations (new product line platforms, modernized underwriting systems): 6-12 months

- Full-scale platform implementations: 12-24 months for the first implementation.

- Gradual MVP patterns: Invariably produce quicker early yields than trying feature-full systems in the beginning.

Selecting the Appropriate Insurance Software Development Company

Your technology choices are as good as your technology partner. In considering an insurance software development company, consider the following:

Insurance Domain Expertise

- Exhibited knowledge of insurance product structure and coverage levels.

- Underwriting and claims procedures in appropriate lines of business.

- Knowledge of regulatory specifications in your target markets.

- Exposure to insurance-specific data models and patterns of integration.

Technical Capabilities

- Experienced with cloud-native architecture and current development practices.

- Powerful API implementation and legacy integration.

- Strong security and compliance engineering practices.

- Automated testing and compliance validation as part of quality assurance.

Delivery Track Record

- Testimonials of clients whose implementations are of the same scope and complexity as yours.

- Cases that illustrate quantifiable business results and not mere technical delivery.

- Clear communication of schedules, risks, and constraints.

- Proven skills in handling multi-stage programs.

Ongoing Partnership Quality

- The ability to support and maintain over the long term, not just during the initial deployment.

- Sensitivity to changing compliance needs.

- Ability to assist you in building up the initial investment as time goes by.

- Defined escalation and service level promises.

Path Forward: Taking Action in 2026

Digitization in the insurance business is a current reality, and the digital divide between those carriers that have and those that have not modernized is expanding by the year. To proceed successfully, the executives need to focus on the following activities:

- Specify what business outcomes are before assessing technology options; define the specific and measurable goals.

- Carry out a sincere legacy evaluation to know where existing systems are truly crippling your business.

- Select an appropriate development model: compare custom, platform, and hybrid models with your strategic needs.

- Choose a partner that has actual insurance knowledge; technical skill alone will not guarantee insurance software development success.

- Budget on constant evolution; consider the first deployment as the start of a process, not the end.

- Implement security and compliance in the early days; it is always more costly and less effective to add these capabilities later.

The kind of decisions you make today regarding the insurance software design, the custom insurance software development strategy, and the technology relationship will determine the competitive position of your organization in the coming years. Carriers with strategic clarity and selection of an appropriate software development company in insurance and discipline in implementation will be the ones that will lead the market in the next decade.