Most teams arrive here because Stripe fees are eating margins, checkout is broken on mobile, or third-party processors don’t cover their market. Often all three.

Statista predicts that the value of digital payment transactions will reach $16.62 trillion by 2028. This is the environment that businesses are competing in. In cases where transaction volume, compliance or UX requirements surpass what an off-the-shelf payment gateway can provide, custom payment gateway development becomes cost-effective.

The Baymard Institute reports that the global cart abandonment rate is 70.19% and 85.65% on mobile. With a custom build, you have maximum control of the checkout process.

Core Features Every Custom Payment Gateway Needs

This is where most conversations go wrong. Teams make a feature list based on what Stripe or PayPal offers, then try to replicate it. That’s not how this works. Your gateway needs to be built around your specific transaction types, your user base, and your regulatory environment. But there are foundational pieces that any production-grade system has to have. Cutting corners on any of them will cost you later.

Secure Payment Processing and Tokenization

The gateway has one absolute job: move money securely. That means encrypting card data in transit and at rest, and replacing raw card numbers with tokens as early in the flow as possible. Tokenization isn’t just good security hygiene. It dramatically reduces your PCI DSS compliance scope, which means lower audit costs and less surface area for a breach.

Sixty percent of merchants already use tokenization, according to industry data. If you’re building new infrastructure and you’re not including this from day one, you’re starting behind.

Multi-Currency and Multi-Method Support

If your customers are in more than one country (and for most digital businesses, they are), your gateway needs to handle local currencies, local payment rails, and local consumer preferences. In Germany, that might mean SEPA direct debit. Brazil relies heavily on Pix for instant payments. In the US, digital wallets dominate the landscape. A gateway that only handles US cards and major digital wallets is already a legacy system.

Digital wallets accounted for 49-56% of global eCommerce transaction value in 2025. Apple Pay and Google Pay are the preferred payment method for 67% of millennial shoppers. Build for this reality from the start, not as an afterthought.

AI-Driven Fraud Detection and Risk Scoring

Global e-commerce fraud losses reached $48 billion in 2023 and the trajectory is getting worse. Financial institutions using machine learning for fraud detection reach 90% accuracy rates. The math is clear. Fraud detection built on real-time behavioral signals, velocity checks, and risk scoring models is not optional infrastructure.

The key architectural decision here is where fraud logic lives. If it’s a plugin or third-party layer added on top of your gateway, it’s slower and leakier than if it’s embedded in the transaction flow itself. Build it in, not on.

Real-Time Transaction Monitoring and Reporting

Merchants need dashboards. Finance teams need reconciliation. Risk teams need alerts. A well-built monitoring layer surfaces transaction performance, failure rates, authorization declines, and anomalies in real time. Not in a report that arrives the next morning when the problem already happened.

Payment Orchestration and Smart Routing

If one acquiring bank is down or returns high decline rates, your system should automatically route to a fallback. Payment orchestration means building logic that dynamically routes transactions based on cost, success rate, geography, or payment method, without any of that being visible to the customer. This is where a lot of custom gateways earn back their development cost: higher authorization rates and lower processing fees through intelligent routing.

Recurring Billing and Subscription Management

When you have a subscription, membership or any other recurring revenue-based business model, you want automated invoice generation, failed payment retry logic, and tax calculation built-in. Adding subscription management to a gateway that was never designed to handle it makes for a system that is very fragile and very difficult to troubleshoot.

RESTful APIs and Developer Documentation

Your gateway will have to integrate with your existing apps, third-party services, accounting systems and virtually any other systems that your operations team uses. The well-documented, clean API isn’t simply developer convenience. It’s the difference between someone in your organisation building a gateway and having to hire a specialist each time they need to add an extra feature.

Feature |

Why It Matters |

Complexity Level |

| Tokenization | Reduces PCI scope, protects card data | Medium |

| AI Fraud Detection | Cuts losses, reduces false positives | High |

| Multi-currency Support | Enables global commerce | Medium-High |

| Payment Orchestration | Improves auth rates, reduces costs | High |

| Recurring Billing | Enables subscription models | Medium |

| Real-time Monitoring | Enables ops and finance oversight | Medium |

| 3D Secure 2.0 | Required for EU (PSD2), reduces fraud | Medium |

| RESTful API | Enables integrations and extensions | Medium |

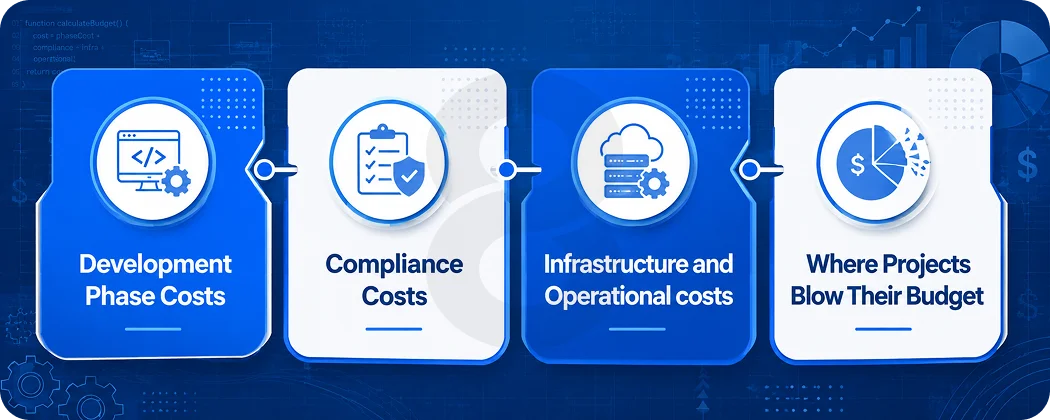

The Real Cost of Payment Gateway Development

The numbers are where a lot of projects stall or go sideways. Here’s a straight read of them.

The range of development costs for a custom payment gateway is from $20,000 to $500,000 or more, depending on the scope, integration level, compliance with global standards, and the processing amounts and currencies you need. Typical mid-market projects are in the $80,000 to $200,000 range for the initial construction. That is, excluding continued expenses.

The initial number is just a part of the story. The issues that plague organizations is the fact that they aren’t prepared for the annual PCI DSS compliance audit, the cost of maintaining the infrastructure, the cost of the fraud prevention tools, and the engineering effort to keep up with the change in regulations.

A breakdown that’s actually useful:

Development Phase Costs

The biggest variable in development cost is scope. A fintech MVP development approach (building just enough to process real transactions securely and learn from them before investing in the full feature set) is a legitimate strategy for startups and growing companies that aren’t yet at enterprise scale. This can get you to a testable, compliant gateway for $30,000 to $80,000.

For a full build with multi-currency support, payment orchestration, custom fraud models, and full API documentation, you’re looking at $120,000 to $300,000 in development alone, assuming a reasonably experienced team.

Compliance Costs

PCI DSS v4.0.1 went into full effect on 1st April 2025. The cost of certification is around $15,000 to $70,000, depending on your scope of compliance. The annual re-certification, penetration testing, and security review costs between $10,000 and $30,000 annually.

Any financial service offering or handling user money? KYC/AML integration could add to API costs and the legal review process.

Infrastructure and Operational costs

Reduce and manage data redundancy, DDoS protection and load handling are lines that are not glaringly obvious, but are very real costs. The cost of the system can range from $2,000 to $15,000 per month, depending on the volume of transactions and the uptime requirements.

Where Projects Blow Their Budget

Almost always, it’s compliance scope creep and underestimated integration work. Teams plan for two banking integrations and end up needing eight. Teams plan for US compliance and then expand to Europe without budgeting for GDPR and PSD2 requirements. The fix is building for extensibility from the start, not retrofitting it.

Build Phase |

Estimated Cost Range |

Timeline |

| MVP Gateway (basic processing) | $20,000 – $80,000 | 3 – 5 months |

| Mid-market Gateway (full features) | $80,000 – $200,000 | 6 – 10 months |

| Enterprise Gateway (global, multi-currency) | $200,000 – $500,000+ | 10 – 18 months |

| PCI DSS Certification | $15,000 – $70,000 | 2 – 4 months |

| Annual Compliance & Maintenance | $25,000 – $80,000/year | Ongoing |

| Cloud Infrastructure | $2,000 – $15,000/month | Ongoing |

Payment Gateway Compliance: What You Actually Need to Know

This section is the one most developers skim. Then they spend six months untangling the consequences.

PCI DSS v4.0.1

PCI DSS v4.0.1 became fully mandatory in April 2025. Only 14.3% of companies achieved full compliance in 2023. Non-compliance penalties run from thousands to hundreds of thousands of dollars, before breach costs.

Compliance scope depends on how the gateway handles card data. Tokenization and hosted payment fields reduce that scope considerably, which is another reason to build those features in from day one.

PSD2 and 3D Secure 2.0

If any of your customers are in the European Union, PSD2 requires Strong Customer Authentication (SCA) for electronic payments. In practice, this means implementing 3D Secure 2.0 authentication, which adds a layer of bank-level verification to the transaction flow without destroying the user experience (when implemented correctly).

Skipping this isn’t just a compliance failure. It’s a liability. Card fraud in the EU exceeded all other payment types in H1 2023. The European Central Bank and national regulators are not lenient about SCA gaps.

GDPR and Data Residency

All personal data of EU citizens (payment data included) falls under GDPR. This impacts storage locations, data retention periods, what can be done with it and how to respond to deletion requests. Data residency needs can have a major influence on your architecture decisions if you deploy infrastructure across multiple regions.

KYC and AML

For platforms that hold user balances, process cross-border transfers, or function as a payment processor rather than a simple gateway, Know Your Customer and Anti-Money Laundering requirements come into play. This typically means third-party identity verification APIs, transaction monitoring, and in some jurisdictions, licensing requirements that need to be sorted out before you write a line of code.

When your product roadmap involves stablecoin payment solutions or any type of crypto-to-fiat settlement, AML obligations become a lot more complicated and differ significantly from one jurisdiction to another. Architecting it in from the start of compliance will be much cheaper than a regulatory finding after launch.

Read More: Cost of Online Payment App in 2026: The Real Breakdown Nobody Gives You

Build vs. Buy: The Honest Framework

The decision tree, without the sales pitch:

You should probably buy (or use a third-party gateway) if you’re processing under $1 million per year, you have a standard product catalog, you’re in a single geography with standard payment methods, and you don’t have the engineering capacity to maintain financial infrastructure.

You should seriously consider building if your transaction fees on third-party platforms are a significant percentage of your gross margin, you need payment methods or checkout flows your current provider doesn’t support, you’re operating across multiple geographies with different regulatory requirements, or your product is itself a payments business.

For companies building custom fintech solutions (platforms where payments are a core part of the product rather than a peripheral feature), the build decision is almost always right. The question becomes when and how, not whether.

The medium-term math usually works like this: paying 2.9% + $0.30 per transaction on a volume of $5 million per year means $145,000+ in processing fees annually. A custom gateway built for $150,000 pays for itself in the first year of operation at that volume. And the business owns the asset going forward.

How to Actually Build a Custom Payment Gateway

This isn’t a step-by-step tutorial. That would take a book. But here’s the architectural and process sequence that teams who get this right tend to follow.

Start with Compliance Architecture, Not Features

The single best piece of advice for anyone starting this project: begin with a compliance-first architecture session before writing a feature list. Map out what card data the system needs to touch, what needs to be stored, and what can be offloaded to hosted fields or tokenization. This determines your PCI scope, which determines a significant chunk of your build complexity and cost.

Everything about data flows, database schemas, logging and monitoring, and infrastructure should be informed by compliance requirements. Building features first and layering compliance on top is how teams end up rebuilding systems from scratch six months later.

Choose Your Tech Stack Deliberately

The backend needs to handle concurrent transactions reliably, recover gracefully from failures, and integrate with banking APIs that have their own quirks and downtime patterns. Node.js, Go, and Java are common choices for the transaction processing layer. PostgreSQL or cloud-native databases for transaction records. Redis for session handling and idempotency key management.

The specific choices matter less than making them deliberately and documenting the reasoning. Teams that pick a stack because it’s fashionable without thinking through transaction safety, retry logic, and failure modes end up with systems that drop payments. Dropped payments are the kind of thing that ends relationships with merchants and users fast.

Build Idempotency in From Day One

This is the detail that separates experienced payment engineers from teams trying this for the first time. An idempotency key ensures that if a network request fails and the client retries, the payment isn’t processed twice. Not building this in from the start means you will double-bill users. It’s not a maybe.

Implement a Sandbox Environment Before Going Near Production

Every payment network (VISA, Mastercard, NPCI for UPI) has a sandbox certification path. Testing shouldn’t stop at the happy path. Slow acquiring bank responses, mid–3D Secure declines, and aggressive retry bursts (like three attempts in two seconds) can all expose hidden weaknesses in the payment flow.

The failure scenarios are where a gateway’s quality is actually measured.

For Teams Building in the Crypto and Stablecoin Space

If a gateway needs to process or settle via stablecoin payment solutions, the architecture needs to treat settlement as a pluggable module rather than a hardwired integration. Visa’s USDC settlement on Solana already reached $3.5 billion in annualized run rate within its first quarter of operation.

The infrastructure for crypto settlement is real and growing. A gateway designed with modular settlement rails can add these capabilities without re-engineering the core transaction flow. One that’s hardwired to traditional card clearing cannot.

This is increasingly relevant for custom software development teams building for global markets where stablecoin settlement offers meaningful advantages in cross-border transaction costs and settlement speed.

Read More: Best Cash Advance Apps: Build Your Own Fintech App

The Developer Experience Problem Nobody Talks About

A poorly documented API is a gateway nobody wants to integrate with. Irfan Ali Baig, Mobile App Lead at 8ration, says the teams that succeed treat API documentation as a product, not a post-launch task.

This matters most when merchants integrate into their own SaaS payment platforms. Clean APIs attract integrations. Cryptic error messages repel them. Webhooks need signed callbacks and a retry queue with exponential backoff built in from day one.