Anyone who’s actually shipped a payment app will tell you that the budget you start with is rarely the budget you end with. Compliance changes mid build. KYC vendors raise prices. Your CTO disappears for two weeks because the sandbox is broken. Welcome to 2026.

If you’re trying to estimate the cost of online payment app development before you commit, you’re already ahead of most founders. Most just sign whatever quote sounds reasonable and hope nothing breaks.

Then it breaks. Usually around month four, right after you’ve burned through the design budget on a settings screen nobody uses. This piece is for the people who want the actual numbers.

Why Payment Apps Still Make Sense in 2026 (Even If You’re Tired)

The global digital payments market is projected to hit $26.89 trillion in transaction value during 2026, with mobile POS payments alone accounting for $18.95 trillion of that figure. That’s not a trend you sit out, even when the venture cycle feels exhausting.

Roughly 5.2 billion people will use digital wallets by the end of 2026, which is more than half of everyone alive with internet access. The U.S. mobile POS market alone is set to clear $1.5 trillion this year. China’s Alipay and WeChat Pay combined cleared over $20 trillion last year.

The bar to actually ship something in this space, though, hasn’t dropped with them. It’s gone up. PCI DSS 4.0 raised the floor on security. Deepfake fraud forced KYC providers to add real time liveness detection. Every regulator wants more logs, more audits, more proof you actually know what you’re doing. None of that is free.

Which is why estimating a real payment app budget matters more than it did even two years ago. You can’t budget for a fintech build the way you’d budget for a basic content app, because the rules have changed. So have the numbers. And the people writing the checks deserve to know that before they sign anything.

Read More: Why Your Business Needs a Blockchain Powered Digital Asset Management System

What Does the Cost of Online Payment App Development Look Like in 2026?

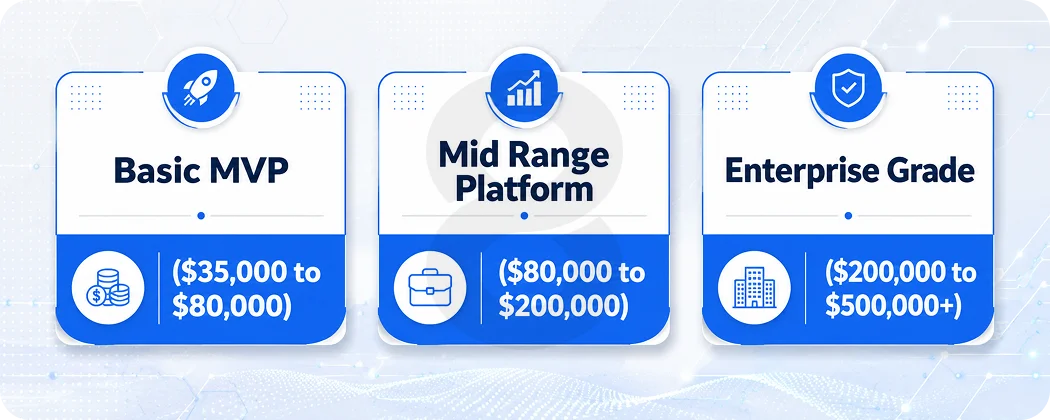

An MVP that respects security and compliance starts around $35,000. A production grade platform with multi currency support, full compliance, and fraud detection that actually catches anything climbs past $400,000.

Most serious builds land between $80,000 and $250,000. And if your quote is way under that range, somebody’s leaving something out and hoping you don’t notice until month four.

Here’s the breakdown most founders need to actually budget against:

App Type |

Estimated Cost |

Timeline |

What You Get |

| Basic MVP | $35,000 to $80,000 | 3 to 5 months | Single currency P2P transfers, light KYC, one payment gateway, basic wallet |

| Mid Range Platform | $80,000 to $200,000 | 5 to 8 months | Multi gateway, full KYC and AML, biometric auth, multi currency, fraud scoring |

| Enterprise Grade | $200,000 to $500,000+ | 9 to 14 months | Banking partnerships, multi region compliance, AI fraud detection, white label panels |

These numbers come from blended estimates across 2026 fintech build data, not from a single vendor quote. Your actual cost will depend on team location, scope creep, regulatory geography, and how often your auditors visit your inbox.

Founders building fintech software for the U.S. and EU markets typically hit the higher end of every range because they’re paying for two parallel compliance regimes.

Where the Money Actually Goes

If you’ve never built a payment app, you’d assume most of the budget goes to building the payment screens. It doesn’t. The payment screens are maybe 10 percent of the real work. The rest is everything you can’t see, and everything regulators care about.

Compliance and security

Compliance is the line item that quietly eats 25 to 40 percent of a real fintech budget. PCI DSS 4.0, GDPR, PSD2 (and the slow shift to PSD3), KYC, AML, and MiCAR if you’re touching crypto. None of these are optional once you handle real money.

The 2025 IBM Cost of a Data Breach Report puts the average financial sector breach at $5.56 million, roughly 25 percent higher than the global average of $4.44 million. The US figure is even sharper at $10.22 million, the highest on record. That’s why your engineering lead won’t let you ship without tokenization, end to end encryption, and proper audit logs.

Compliance integration with KYC vendors like Sumsub, Onfido, or Alloy alone runs $15,000 to $30,000 just to implement, before you pay per verification. For the actual standards your auditor will hold you to, the PCI Security Standards Council documentation is the source of truth.

Feature scope and the creep that kills you

Every founder thinks they need everything in version one. They don’t. Nobody does. What actually matters at launch is user onboarding, identity verification, one payment rail that works, a wallet, and a transaction history people can scroll through without crying. That’s it.

Everything else you’re convinced is essential can wait until you have users who are asking for it, which, fair warning, is going to be a smaller and slower group than your deck suggests.

Scope creep doesn’t usually arrive as a big request. It arrives as ten small ones over two months. Add both Apple and Google Pay, referral system, and chat support widget. Each looks small in isolation. Together they add three months and $40,000 you didn’t plan for.

Where your team sits

Rates are all over the place and have been for years. A senior fintech engineer stateside will run you somewhere between $140 and $200 an hour, sometimes more if they’ve shipped something a VC has heard of.

Same level of talent in Pakistan, India, or parts of Eastern Europe sits closer to $30 to $70. Western Europe is the awkward middle, $80 to $120, where you pay almost American prices without quite getting American time zones.

None of these numbers actually tells you who’s going to ship a working product, which is the part that took me years to internalize.

Most U.S. fintech founders end up running a hybrid model. Product leadership stateside, engineering offshore. Done right, that cuts your build cost by 40 to 55 percent compared to an all U.S. team.

Done badly, you spend three months explaining timezone overlap and ship nothing. Vetting matters more than rate. A cheap team that has never shipped a regulated product will cost you more in rewrites than a slightly pricier one that has.

Native or cross platform

iOS and Android native still wins on raw performance and tight hardware integration, which matters for biometric auth and NFC payments. But cross platform app development with React Native or Flutter cuts your cost by 30 to 40 percent, and the gap on real world performance has nearly closed for typical payment use cases.

If you’re a startup, cross platform is almost always the right call. If you’re shipping a high security crypto wallet or anything that pushes the hardware, native is still worth the premium.

Third party APIs and SDKs

Stripe, Plaid, Twilio, Sumsub, Google Maps, Firebase. Every payment app integrates a dozen vendors. Implementation cost is one thing. The monthly bills are another, and they scale with your users. More on that further down.

Read More: Digital Wallet Solutions: Complete Guide for Startups in 2026

Feature by Feature Cost Breakdown

Some features matter at launch. Most don’t. Here’s where the budget actually gets eaten by scope.

Feature |

MVP Version |

Advanced Version |

Additional Cost |

| User Onboarding and KYC | Email and phone, basic ID upload | Biometric liveness, document AI, address verification | $15,000 to $30,000 |

| Payment Processing | Single gateway, card and bank transfer | Multi gateway, BNPL, wallet, crypto | $10,000 to $25,000 |

| Wallet System | Single currency wallet | Multi currency, auto convert, ledger system | $12,000 to $28,000 |

| Authentication | Password and OTP | Biometric, device binding, MFA | $5,000 to $15,000 |

| Transaction Limits and Fraud | Basic rule engine | ML fraud scoring, behavior analysis | $20,000 to $50,000 |

| Notifications | Push and email | In app chat, AI assistant, transaction insights | $8,000 to $18,000 |

| Reporting and Analytics | Basic transaction history | Real time dashboards, predictive analytics | $10,000 to $25,000 |

| Admin Panel | Basic user and transaction management | Full ops console, compliance workflows | $15,000 to $35,000 |

If you’re targeting a mobile banking app experience or anything that touches real funds in real accounts, expect to land in the advanced version of most rows. There’s no halfway version of compliance. Either you meet the standard or you don’t ship.

For founders building toward stablecoin rails, on chain settlement, or crypto wallets, blockchain development adds another category of cost.

Smart contract audits alone run $15,000 to $50,000 per contract, and you’ll need at least two independent ones before any sane investor or banking partner trusts your wallet.

The Hidden Costs Most Quotes Leave Out

The quote you sign is rarely the bill you actually pay. Here’s what shows up after launch that nobody mentions during the sales process.

Cloud infrastructure

Ten thousand monthly active users will cost you roughly $800 to $2,500 a month on AWS or GCP. Push that to a hundred thousand and you’re at $5K to $15K. Hit a million and you’re easily clearing $20K, and none of those numbers include geographic redundancy or disaster recovery yet.

Founders cut those two line items every single time because nothing has broken yet and the bill already feels too big. Then one regional outage takes you offline for nine hours on a Tuesday, support is on fire, your investor texts you, and you go back and pay for the thing you should have paid for in month two.

Vendor and API fees

This is the one that stings. Stripe takes 2.9 percent plus $0.30 per transaction. On $200,000 in monthly transaction volume, that’s $5,800 in processing fees alone.

Plaid for bank linking is $0.30 to $1.50 per linked account. Sumsub for KYC is $1 to $3 per verification. Twilio SMS at scale runs $300 to $1,500 a month. Google Maps if you do merchant locations adds $500 or more at scale.

You wake up six months in and realize your vendor spend is higher than your engineering team’s salary. That’s fintech. The companies that survive it plan for it from month one and design every flow to minimize per call costs.

How to Reduce the Cost of Online Payment App Development Without Killing the Product

You can cut the cost of online payment app development by 30 to 50 percent without compromising what matters. Here’s how, written by someone who has watched founders do both versions of this.

Ship a real MVP, not a “MVP.” That means one currency, one payment rail, one user type. Validate that people actually transact through your product before you spend on multi currency wallets or merchant onboarding.

Use composable infrastructure. Plaid for bank data, Stripe for processing, Sumsub for KYC, Twilio for messaging. Building any of these from scratch costs five times more than integrating them and gives you exactly nothing competitive at launch.

Pick cross platform unless you have a hard reason not to. The 30 to 40 percent savings is real, and modern Flutter and React Native handle payment flows fine. Save native for the screens that genuinely need it, if any.

Vet your engineering partner like your runway depends on it, because it does. Live portfolio of shipped fintech products, real client references you can call, clear IP transfer language in the contract.

If they can’t show you a payment app they shipped that’s live in an app store right now, walk away. There’s no learning curve discount that’s worth paying for in regulated work.

Don’t bolt on compliance. Build PCI DSS architecture, audit logging, and encryption from sprint one. Retrofitting compliance after launch typically costs two to three times more than building it in.

Read More: Best Crypto Apps to Kickstart Your Blockchain Venture

How Long Does It Take to Build a Payment App in 2026?

Phase |

Basic MVP |

Mid Range |

Enterprise |

| Discovery and Planning | 2 to 3 weeks | 3 to 4 weeks | 4 to 6 weeks |

| UI/UX Design | 3 to 4 weeks | 4 to 6 weeks | 6 to 10 weeks |

| Core Development | 10 to 14 weeks | 16 to 24 weeks | 26 to 40 weeks |

| Compliance and Security Integration | 3 to 5 weeks | 6 to 10 weeks | 10 to 16 weeks |

| QA and Penetration Testing | 3 to 4 weeks | 4 to 6 weeks | 6 to 10 weeks |

| Deployment and Audits | 2 to 3 weeks | 3 to 5 weeks | 4 to 8 weeks |

| Total | 4 to 6 months | 7 to 10 months | 12 to 18 months |

Add 2 to 4 weeks for app store review, another 2 to 6 weeks for payment gateway approval (Stripe and Adyen are usually fast, banking partners are not), and another 4 to 8 weeks for PCI DSS Level 1 certification if you need it.

None of these run in parallel reliably. Budget the calendar honestly or watch your launch date drift by a quarter.

Read More: Top Banking Software Solutions to Modernize Your Financial Services in 2026

Why Working With the Right Partner Matters More Than the Hourly Rate

The cheapest team is rarely the cheapest project. We’ve watched founders pay $40,000 for a “complete payment app” only to spend another $120,000 fixing security holes and rebuilding the wallet logic six months later. That math works for nobody except the original vendor.

A specialized mobile app development partner that has actually shipped regulated products knows what to argue with you about.

They’ll push back when you ask for features you don’t need. Expect them to insist on logging architecture before you think it’s necessary. The first sprint will feel slower, but every sprint after gets faster, because they’re not stopping every two days to figure out something they’ve already done ten times.

That’s the partnership most founders need and don’t know how to find until they’ve already burned through one or two bad ones.

Read More: Fintech App Development Cost in 2026: Full Breakdown by Feature, Team & Region