Cash did not die quietly. It got replaced by something faster, smarter, and already in 5.2 billion pockets worldwide. Yet most startups are still building payment experiences that belong in 2019. That gap is not just a product problem. It is a revenue problem.

Today’s users do not wait for clunky checkout flows to improve. They leave. And with digital wallets capturing 53% of all global online purchases in 2025, the startups winning are the ones that treated payments as a core product decision, not a last-minute integration.

This guide covers everything: wallet types, must-have features, tech stack, compliance, and real build costs. Let’s get into it.

What Are Digital Wallet Solutions, and Why Do They Matter Right Now?

A digital wallet is a software system that stores payment credentials, processes peer-to-peer and merchant transactions, manages transaction history, and supports loyalty programs, crypto banking features through a mobile app, web interface, or both.

The market momentum behind this technology is impossible to ignore. The global digital wallet market is projected to reach $68.02 billion in 2026, while digital wallets have already captured 53% of all global online purchases, more than double credit cards.

These are not future projections. These are today’s conditions. If your product touches payments in any form, building on digital wallet infrastructure is no longer optional.

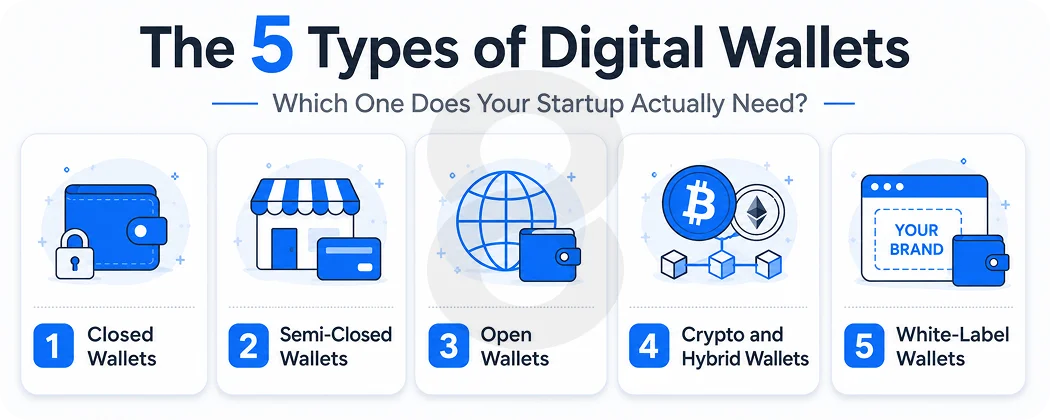

The 5 Types of Digital Wallets: Which One Does Your Startup Actually Need?

Before you write a single line of code, you need to answer one foundational question: what kind of wallet are you building? Each type comes with different technical requirements, compliance obligations, and go-to-market timelines.

1. Closed Wallets

A closed wallet operates entirely within your own ecosystem. Users load funds and spend them exclusively with your platform. Think of a food delivery app that lets users top up a balance and pay for orders.

Closed wallets carry the lowest regulatory burden and the fastest time to market. However, they also offer the least flexibility for users, which can become a retention challenge as your platform scales.

2. Semi-Closed Wallets

Semi-closed wallets are accepted across multiple merchants who have a formal agreement with the wallet provider. This is the PayPal and Paytm model. These wallets require a payment aggregator partnership and a somewhat higher compliance lift, but they offer significantly more value to users.

For startups targeting a specific vertical, such as healthcare, logistics, or retail, a semi-closed model often hits the sweet spot between regulatory simplicity and user utility.

3. Open Wallets

Open wallets are bank-linked and enable full financial functionality: withdrawals, transfers, bill payments, and purchases anywhere. They carry the highest compliance requirements and generally require licensing.

However, they also deliver the maximum lifetime value per user, which is why most neobanks and fintech-first startups aim here eventually. Building a robust mobile banking app in this category demands strong backend architecture and a compliance-first development approach from the very beginning.

4. Crypto and Hybrid Wallets

Crypto wallets store, send, and receive digital assets. Hybrid wallets combine fiat and crypto functionality in a single interface. Global crypto transaction volume is projected to reach $10.8 trillion in 2025, highlighting stronger integration between crypto and digital wallets.

For startups operating in Web3, DeFi, or cross-border remittances, a hybrid wallet built on reliable blockchain fintech solutions is increasingly the product that investors and users want.

5. White-Label Wallets

White-label wallets are pre-built, brandable payment infrastructures that you configure and deploy under your own brand. They are the fastest path to market, often cutting time to launch from months to weeks.

The trade-off is limited differentiation and less control over the roadmap. For startups validating a concept or entering a new market, white-label is often the smartest first move before investing in a fully custom build.

Read More: How to Get a Crypto Wallet and Secure Your Digital Assets

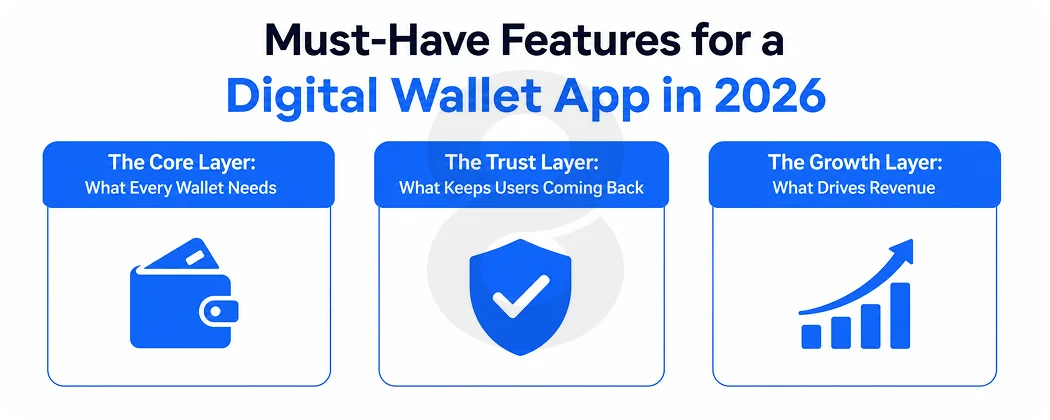

Must-Have Features for a Digital Wallet App in 2026

The feature gap between a wallet users trust and one they abandon is smaller than most founders expect. It comes down to three layers.

The Core Layer: What Every Wallet Needs

Your foundation must include secure user registration with KYC (Know Your Customer) verification, bank account and card linking via APIs like Plaid or Stripe, peer-to-peer transfers, real-time transaction history, push notifications for every transaction, and multi-currency support if you are targeting international users. These are not differentiators. They are the baseline.

The Trust Layer: What Keeps Users Coming Back

Security is not a feature you add later. Digital payment fraud losses are projected to exceed $50 billion in 2025, yet AI-powered detection systems have reduced losses by 30% at institutions using them.

Your trust layer should include biometric authentication (Face ID, fingerprint), two-factor authentication, end-to-end AES-256 encryption, real-time fraud detection, and full PCI-DSS compliance. Users who trust your wallet tell their friends. Users who do not, never come back.

The Growth Layer: What Drives Revenue

Once users trust your wallet, the growth layer is what monetizes them over time. This includes cashback and loyalty programs, in-app spending analytics, QR code payment support, bill payment integration, and referral programs with wallet-based incentives.

QR code payments emerged as the most widely used digital wallet transaction method in 2026, with 380 billion transactions recorded globally and making up more than 40% of all transactions by volume. If your wallet does not support QR payments in 2026, you are missing the dominant transaction method on the planet.

Read More: 30 Best Cryptocurrency Wallet Apps for 2026

The Tech Stack Behind High-Performance Digital Wallets

Getting your architecture right at the start will save you from costly rewrites six months in. Here is what a production-grade wallet stack looks like in 2026.

- Frontend: React Native or Flutter for mobile delivers the best performance-to-development-cost ratio for startups. Both are excellent choices for cross-platform wallet apps that need to run flawlessly on iOS and Android without maintaining two separate codebases. React.js handles web dashboard needs well.

- Backend: Node.js or Python (using Django or FastAPI) powers scalable, high-throughput financial APIs. For transaction-heavy platforms processing thousands of requests per second, Go is also worth considering.

- Database: PostgreSQL handles relational transactional data reliably. Redis handles session management and caching, which keeps response times fast even under load.

- Security Architecture: AES-256 encryption for data at rest, TLS 1.3 for data in transit, OAuth 2.0 for authentication flows, and tokenization for all payment credentials.

- Payment APIs: Stripe Connect for card processing, Plaid for bank account linking in North America, and regional payment gateways depending on your launch markets.

- Blockchain Layer: For crypto-enabled wallets, Ethereum, Solana, and Hyperledger each offer different trade-offs around transaction speed, cost, and smart contract capability. The right choice depends entirely on your use case, which is exactly why having an experienced fintech app development partner matters here.

All of this needs to be designed as a modular, microservices-based architecture. Monolithic wallet apps are technical debt from day one. Build for scale from the start, even if you are starting with a narrow MVP.

Read More: Best Crypto Apps to Kickstart Your Blockchain Venture

How Much Does It Cost to Build a Digital Wallet App in 2026?

Cost depends on scope, complexity, compliance requirements, and the expertise of your development partner. Here is a realistic framework.

| Build Scope | Timeline | Estimated Cost Range |

| MVP (core P2P, top-up, history) | 8 to 12 weeks | $20,000 to $40,000 |

| Standard wallet with KYC and fraud detection | 4 to 5 months | $50,000 to $90,000 |

| Full-featured fintech platform | 6 to 12 months | $100,000 to $200,000+ |

The variables that push cost upward include the number of payment gateway integrations, the depth of compliance architecture required, whether you need a web dashboard alongside the mobile app, and the complexity of your blockchain or crypto layer if applicable.

The variables that pull cost down include starting with white-label infrastructure for your MVP, limiting your initial launch to a single market, and choosing a proven development partner who has built fintech products before and does not learn on your budget. For a project-specific estimate, use 8ration’s app cost calculator to get a scoped number in minutes.

The 3 Mistakes That Kill Fintech Startups Before They Scale

After working on fintech products across North America, the Middle East, and Asia, we see the same three patterns repeatedly.

Treating Security as a Feature Rather Than a Foundation

Security cannot be an afterthought in fintech. When you layer protection onto a product after launch, you are essentially putting a lock on a door with no walls.

One exposed API endpoint, one unencrypted data store, or one missed compliance requirement is enough to permanently damage user trust and shut your startup down. Security architecture belongs in sprint zero, full stop.

Building Everything Before Validating Anything

Startups consistently overbuild before they know what users actually want. Launch a focused MVP with core wallet functionality, then let real user behavior tell you what to add next.

Spending $150,000 on loyalty programs and investment modules before confirming users even engage with your core transfer feature is one of the most common and expensive mistakes in fintech product development.

Choosing a Development Partner Based on Hourly Rate Alone

Fintech is technically and legally unforgiving. A team that misses a KYC requirement or ships a tokenization vulnerability will cost you far more to fix than whatever you saved on the initial contract.

The right development partner brings a traceable fintech portfolio, honest answers about compliance architecture, and accountability that extends well beyond your product’s launch day.

Read More: Best Cash Advance Apps: Build Your Own Fintech App

Why Startups Build Digital Wallets with 8ration

Building a fintech product is hard. Building one that scales, stays compliant, and actually converts users is harder. That is exactly where 8ration comes in.

Our fintech and blockchain practice covers everything from fintech mobile apps and crypto-enabled hybrid wallets to enterprise-grade open platforms and custom payment software. We have built it before, across multiple markets and regulatory environments.

Final Thoughts!

The market is not pausing for anyone. By 2030, the global digital wallet market is forecast to reach $145.35 billion, growing at a 20.9% CAGR. The startups winning that market are building now, with the right architecture, the right compliance foundation, and the right team.

You do not need to build everything at once. Start lean, validate fast, and scale from a solid foundation. What you do need is a team that has been here before. 8ration has. Let’s build.