Here’s the thing about building a payment app. You start with a clean mental image: users open the app, tap send, money moves. Then your first backend developer asks “have you thought about idempotency keys?” and you realize that’s an entire system design problem.

According to Statista, the global digital payments market is projected to reach $36.09 trillion by 2030, with 4.5 billion digital wallet users already active. The opportunity is enormous, but you have to build it right. This guide walks through features, architecture, compliance, tech stack, and the mistakes teams keep making.

Why the Online Payment App Market Still Has Room for You

Before we get into the technical side, it’s worth grounding this in why anyone would even attempt to build something in a space where PayPal, Stripe, Venmo, and Apple Pay already exist.

The answer is almost always one of three things: a specific vertical that existing apps don’t serve well, a geography where current solutions aren’t localized, or a feature set that a business needs to own rather than rent from a third party.

The numbers support this framing. According to Coinlaw‘s digital payments forecast, Mobile POS Payments alone is projected to reach $18.95 trillion in transaction value in 2026, making it the single largest segment within digital payments. And that’s before you factor in peer-to-peer transfers, B2B payments, BNPL integrations, and cross-border remittances.

In the US, 43% of consumers reported using a digital wallet in-store in 2024, up from just 23% in 2019. That’s not a slow adoption curve. That’s a generational shift that’s still in the middle of happening. There’s real room to build here, but only if you understand what “building” actually means in the context of financial software.

Read More: Custom Online Payment Gateway Development: Features, Cost, and Compliance Guide

What Features Does a Payment App Actually Need?

This is where most product teams go wrong. They build a feature list that looks like a marketing page, not a technical specification. “One-click payments” sounds great in a deck, but it implies a whole chain of systems that need to work in concert: tokenized card storage, user session management, idempotent transaction processing, real-time authorization, and settlement reconciliation.

Here’s how to think about features in layers:

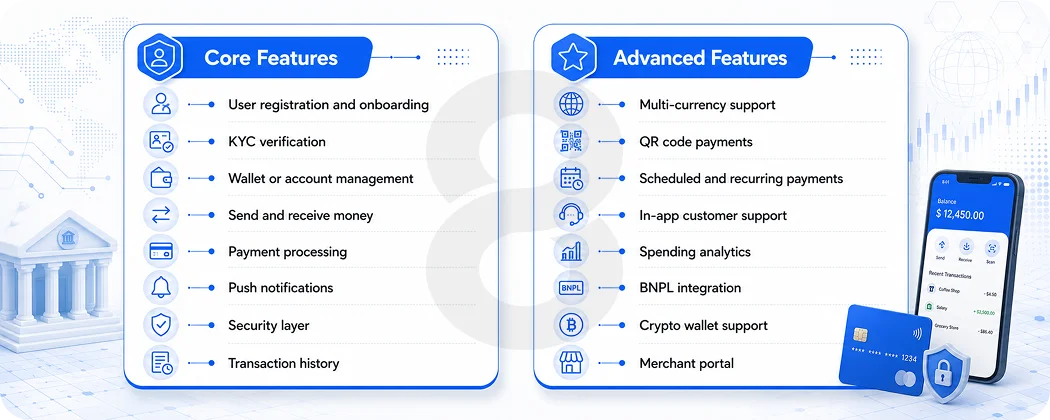

Core Features Every Payment App must have

| Feature | What it actually involves |

|---|---|

| User registration and onboarding | Email/phone verification, secure password storage, session management |

| KYC verification | Identity document upload, liveness check, third-party verification (Sumsub, Onfido) |

| Wallet or account management | Balance display, linked bank accounts or cards, transaction history |

| Send and receive money | P2P transfers, request money flows, split bill logic |

| Payment processing | Gateway integration (Stripe, Adyen, Braintree), authorization, capture, refunds |

| Push notifications | Real-time transaction alerts, fraud warnings, balance updates |

| Security layer | 2FA, biometric login, session timeout, device fingerprinting |

| Transaction history | Searchable log with status, timestamps, merchant info, downloadable receipts |

Advanced Features that Create Differentiation

| Feature | Business rationale |

|---|---|

| Multi-currency support | Essential for cross-border use cases |

| QR code payments | Growing fast, especially in emerging markets |

| Scheduled and recurring payments | Subscription businesses need this |

| In-app customer support | Reduces churn after a failed transaction |

| Spending analytics | Increases retention and perceived value |

| BNPL integration | High demand in US and UK markets |

| Crypto wallet support | Growing segment, adds complexity |

| Merchant portal | If you’re building a two-sided platform |

The honest advice here is to start with the minimum set that lets you actually process a transaction end to end, securely and compliantly. Everything else is iteration.

The Architecture Behind a Payment App (And Why It’s More Complex Than You Think)

If you’ve built consumer apps before, you’re used to thinking about architecture in terms of UI performance and database load times. Payment app architecture adds several layers on top of that, and some of them are non-negotiable from day one.

Microservices vs. monolith

For a payment app with any meaningful scale expectations, a microservices architecture is almost always the right call. Here’s why: payment systems have components with very different security requirements, scaling requirements, and failure modes. Your transaction processing service should not live in the same codebase as your notification service or your user authentication layer.

Event-driven messaging systems, specifically Apache Kafka or RabbitMQ, are typically used to coordinate between services. When a transaction is initiated, an event fires. The authorization service picks it up, processes it, and fires another event. The notification service picks that up and sends the push alert. The reconciliation service logs it. Each component does one thing independently, and the whole system is resilient to partial failures.

The Layers of a Payment App Architecture

Frontend layer

Your mobile clients (iOS and Android) or web clients communicate with your API gateway. React Native and Flutter are the most common cross-platform choices, though Swift for iOS and Kotlin for Android still offer performance advantages for complex payment flows.

API gateway

A single entry point that handles authentication, rate limiting, and request routing. This is where your JWT token validation happens before any request touches your business logic.

Core services layer

This is where your actual payment logic lives:

- Transaction service (initiates, tracks, and settles payments)

- User service (account management, authentication)

- KYC service (identity verification orchestration)

- Fraud detection service (real-time risk scoring)

- Notification service (push, SMS, email)

- Wallet service (balance management, reconciliation)

Payment gateway integration layer

Your app doesn’t process card transactions directly. You integrate with a payment processor, Stripe, Adyen, Braintree, or a direct banking API, through a dedicated integration layer that handles retry logic, error handling, and webhook processing.

Database layer

Most production payment apps use a combination of relational databases (PostgreSQL) for transactional data that needs ACID compliance and Redis for caching and session management. Some teams add Cassandra or MongoDB for high-volume event logs.

Security and compliance layer

Encryption at rest, encryption in transit (TLS 1.3 minimum), tokenization of sensitive card data, audit logging for every state change, and an immutable transaction ledger.

The Clearing and Settlement system

This is the piece that most product teams underestimate. When a user sends $50, the money doesn’t just teleport. There’s authorization (is this transaction approved?), clearing (settling what’s owed between banks), and settlement (actual fund movement).

Building or integrating a robust clearing and settlement system requires designing for reconciliation, meaning automated processes that catch discrepancies between what your ledger says happened and what the bank says happened.

Compliance Is Not a Phase. It’s a Foundation

This is where teams burn the most time and money after the fact. KYC, AML, and PCI DSS are not features you add to a payment app. They’re properties of how the app is built from the ground up.

KYC (Know Your Customer)

Every user who wants to move money beyond basic thresholds needs to be verified. In practice, this means collecting government ID, running liveness detection to confirm it’s a real person, and checking the result against sanctions lists (OFAC, UN, EU watchlists). Services like Sumsub and Onfido handle the verification workflow. Your app needs to orchestrate the flow, store the verification status, and surface it correctly in your transaction logic.

Worth noting: deepfake fraud grew over 1,100% in the US in early 2025. Standard selfie-plus-ID verification is no longer sufficient for high-risk flows. Biometric liveness detection using micro-expression analysis is becoming the new baseline.

AML (Anti-Money Laundering)

AML controls require your transaction monitoring system to flag unusual patterns automatically: unusually large transactions, rapid movement of funds through multiple accounts, transactions to high-risk geographies. You’re not just logging transactions; you’re analyzing them in real time against risk models and filing Suspicious Activity Reports (SARs) when thresholds are crossed.

PCI DSS

If your app touches card data at any point, you’re in scope for PCI DSS. The most common approach is to minimize your scope by integrating with a PCI-compliant processor (Stripe, Adyen) and using tokenization so that actual card numbers never touch your servers. Even with tokenization, you still need to maintain compliant network security, access controls, and audit logging.

Failing to comply with AML and KYC regulations can result in severe penalties from regulators like FinCEN (US), FCA (UK), and the EU AML Authority, including business shutdowns. This is not theoretical. It happens to funded startups with real products.

Read More: Cost of Online Payment App in 2026: The Real Breakdown Nobody Gives You

The Development Process, Honestly

A lot of guides present payment app development as a clean, sequential process. In reality, it’s messier. Regulatory feedback loops affect your architecture. Third-party API documentation is sometimes wrong. Your banking partner takes six weeks to respond to an integration question.

Here’s how it actually tends to go:

Phase 1: Discovery and compliance mapping (4 to 6 weeks)

Before anything gets designed or coded, you need to know:

- What jurisdictions are you operating in?

- What licenses do you need, and how long do they take to obtain?

- Which regulatory standards apply (PCI DSS, GDPR, CCPA, PSD2, local equivalents)?

- What are your monetization mechanics (transaction fees, subscription, interchange sharing)?

The team working on your mobile app development needs to be involved in these conversations, not brought in later. Architecture decisions flow from regulatory requirements, not the other way around.

Phase 2: Architecture design and tech stack selection (3 to 4 weeks)

Select your payment processor integration (Stripe for most markets, Adyen for enterprise and multi-currency). Choose your backend language (Node.js with TypeScript is popular for its API-friendly ecosystem; Java/Spring for teams that need enterprise-grade stability; Python for teams with strong data science ambitions on the fraud detection side). Pick your messaging system, database strategy, and cloud provider (AWS is the most common choice for fintech due to its compliance certifications).

This is also when you build your security architecture: encryption strategy, token vault setup, audit log schema, and API authentication flows.

Phase 3: UI/UX design (4 to 6 weeks)

Payment flows are high-anxiety moments for users. Every extra tap, every ambiguous confirmation screen, every error message that doesn’t explain what went wrong creates friction that costs you transaction completion rate and retention. The design process for a payment app isn’t just aesthetics. It’s error state design, empty state design, trust-building visual language, and accessibility compliance. Teams that specialize in UI/UX design for financial products understand that the “are you sure?” screen is as important as the home dashboard.

Phase 4: Backend development (12 to 20 weeks)

This is where most of the budget goes. You’re building:

- User authentication and session management

- KYC flow orchestration with third-party verification

- Core transaction processing logic with proper idempotency

- Payment gateway integration with retry logic, webhook handling, and reconciliation

- Real-time fraud detection hooks

- Clearing and settlement workflows

- Admin and reporting tools

The backend of a payment app is not a CRUD application. Every endpoint that touches money needs to be idempotent, meaning if the same request fires twice (which happens during network failures), the system handles it correctly rather than double-charging or double-crediting.

Phase 5: Frontend development (8 to 12 weeks)

Mobile clients are built in parallel with backend development. The frontend work involves building every screen and flow, integrating with your backend APIs, implementing biometric authentication (Face ID, fingerprint), handling real-time push notifications, and testing across device types and OS versions. Teams that understand cross-platform development can significantly reduce the time and cost of shipping on both iOS and Android simultaneously.

Phase 6: Security testing and compliance audit (4 to 6 weeks)

Before launch, your app needs penetration testing by an external security firm, vulnerability scanning across your API surface, PCI DSS compliance verification if you’re in card scope, and functional testing across every transaction flow and failure scenario. This phase is not optional and cannot be compressed. A payment app with an unpatched security vulnerability is a liability, not a product.

Phase 7: Soft launch and iteration (ongoing)

Most successful payment apps launch to a limited user base first: a closed beta, a single geography, or a single user type. This lets you watch real transaction flows, catch reconciliation issues, tune your fraud model, and load test your infrastructure before you’re managing scale.

Tech Stack Reference for Payment App Development

Here’s a practical overview of what teams actually use in production:

| Layer | Options | Why Choose It |

|---|---|---|

| Mobile (iOS) | Swift, React Native, Flutter | Swift for native performance; React Native for faster cross-platform development |

| Mobile (Android) | Kotlin, React Native, Flutter | Kotlin preferred for native apps; Flutter gaining popularity for cross-platform projects |

| Backend | Node.js/TypeScript, Java/Spring, Python | Node.js for API-heavy workloads; Java for large-scale enterprise systems |

| Database (Primary) | PostgreSQL | ACID compliance is essential for financial transaction data |

| Database (Cache) | Redis | Supports session management, rate limiting, and high-speed caching |

| Message Queue | Apache Kafka, RabbitMQ | Enables event-driven transaction processing and scalability |

| Payment Gateway | Stripe, Adyen, Braintree | Stripe suits most startups; Adyen excels in enterprise multi-currency environments |

| KYC Provider | Sumsub, Onfido | Both provide API-first identity verification workflows |

| Cloud Infrastructure | AWS, GCP | AWS is widely adopted in fintech due to extensive compliance and security tooling |

| Fraud Detection | Custom ML Models, Sift, Kount | Sift and Kount accelerate launch; custom models become valuable at scale |

| Monitoring | Datadog, New Relic | Real-time observability is critical for financial system reliability and compliance |

What It Actually Costs to Build a Payment App

The range here is genuinely wide and the “it depends” answer is legitimately correct.

| App Type | Estimated Cost | Timeline |

|---|---|---|

| MVP (Basic P2P + KYC + One Gateway) | $50,000 – $120,000 | 4 – 6 months |

| Mid-Market (Multi-Currency, Advanced Fraud Detection, Merchant Features) | $150,000 – $400,000 | 8 – 14 months |

| Enterprise-Grade (Full Compliance Stack, Multiple Jurisdictions, Custom Gateway) | $400,000 – $600,000+ | 14 – 18+ months |

Geography affects rates significantly. US-based development teams typically charge $100 to $150 per hour. Eastern European teams average $60 to $75 per hour. The right choice depends on your timeline, communication needs, and the specific expertise required for financial software.

One honest note: teams that include engineers experienced with fintech regulations and financial data architecture from the start almost always ship faster and cheaper than teams that learn these things mid-build. Investing in the right custom software development partner at the beginning tends to cost less than fixing compliance gaps after launch.

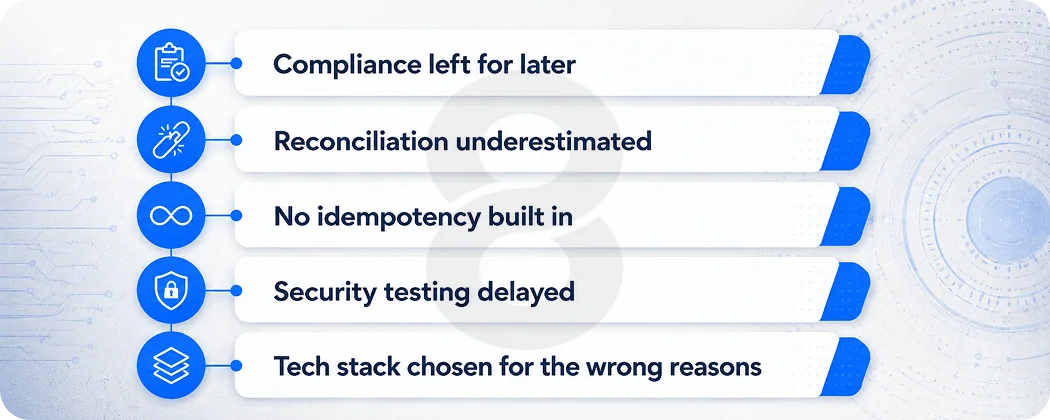

The Mistakes Teams Keep Making

Most payment app failures aren’t technical. They’re process failures that compound quietly until they’re too expensive to ignore. Here are the five that show up constantly.

Compliance left for later

KYC and AML requirements shape your data model, your onboarding flow, and your ability to operate in certain markets. Teams that treat them as an afterthought end up rebuilding core systems in production, which is never cheap.

Reconciliation underestimated

Every mismatch between your internal ledger and the bank’s records needs to be caught and resolved automatically. Teams that skip this initially spend months debugging discrepancies manually, often while real money is sitting unaccounted for.

No idempotency built in

Network failures during transactions are not edge cases. They happen constantly at scale. If your transaction service processes the same request twice without detecting it, you will double-charge users and spend weeks cleaning it up.

Security testing delayed

Finding a vulnerability in a penetration test six months into development is painful. Finding it after launch is a liability. Security architecture decisions are always cheaper to fix before production code is written.

Tech stack chosen for the wrong reasons

The best tech stack is the one your team actually knows. Chasing trends in a financial product leads to slower delivery, harder debugging, and security gaps that only surface once real user funds are involved.