Ask any growing business who actually owns the payment system and watch the room go quiet. Finance assumes it belongs to the developers. The developers assume it came with a gateway contract someone signed years ago.

That mess has a fix. Integrated payment solutions merge payment processing with the software your business already runs on. Money comes in, and every connected system updates on its own.

Nobody retypes anything, nobody spends month-end on reconciliation marathons, and the mystery gap between what the bank says and what the books say finally closes.

There is also a scale problem that keeps getting bigger. Statista expects global digital payment transaction value to hit $37.45 trillion in 2026. That figure sounds abstract until a customer tries to pay in a way your setup does not support, then walks.

Disconnected payment systems bill a business twice for the same weakness. The first invoice arrives as staff hours spent moving data by hand. The second never arrives at all, because it is the sale that quietly went to someone else.

The rest of this guide breaks down how integrated payments actually work, where the savings hide, and what the revenue upside looks like in practice.

What Integrated Payment Solutions Are and How They Work

An integrated payment solution builds payment processing into the software a business already lives in. Once that connection exists, the payment stops being its own chore. A customer pays, and the transaction writes itself into accounting, inventory, and the customer’s record in the same moment, with nobody copying numbers between screens.

The old setup worked very differently. A standalone terminal took the card and went silent. Days later someone sat down to match batch reports against sales records, while someone else adjusted stock counts by hand. Each of those handoffs invited a delay or a typo, and usually got one.

How standalone payments differ from integrated payments

Standalone payment processing treats the transaction as an island. The terminal or gateway does one job. It moves money. Everything around it stays manual.

Integrated payments treat every transaction as information, not just money movement. The moment a payment lands, the ledger updates, stock adjusts, and the customer’s purchase history gains a new line. Reports stay current on their own, with no one pulling exports at month end.

The practical difference shows up at month end. One approach means days of reconciliation. The other means the books already match.

How payment integration works behind the scenes

APIs make all of this possible. An application programming interface is basically a messenger between systems, and in payments it carries transaction data from the gateway and processor into every tool a business runs. One payment sends one message, and every connected system hears it at once.

Four pieces do most of the work:

- Payment gateway: It captures and encrypts payment details at checkout, whether that happens online or at a counter.

- Payment processor: It moves the transaction between the customer’s bank and yours for authorization and settlement.

- APIs and SDKs: They connect the gateway and processor to your POS, app, or custom software so data travels without help.

- Tokenization and encryption: Card numbers become useless tokens, so sensitive data never sits on your servers.

Security rules keep the whole chain honest. Any system that touches card data has to meet PCI DSS requirements, the global standard for protecting cardholder information. With a properly built integration, the provider carries most of that weight instead of your team.

Read More: How to Build an Online Payment App: Features, Architecture, and Development Process

The Hidden Costs of Non-Integrated Payment Processing

Nobody budgets for the cost of disconnected payments. It hides in salaries, refunds, and quiet errors. Then one day a founder adds it up and feels sick.

Here is where the money actually leaks.

Manual reconciliation burns paid hours

Every transaction entered twice is labor spent on nothing. A bookkeeper matching gateway reports against bank deposits does work a machine should do. Multiply that by hundreds of transactions a month. Then multiply by twelve.

Businesses rarely track this cost because it hides inside existing salaries. That does not make it free. It makes it invisible.

Errors compound quietly

Manual entry produces typos. Typos produce mismatched records. Mismatched records produce refund disputes, tax headaches, and inventory counts that lie. Each error costs little on its own. Together they erode margins and trust in your own numbers.

Your data lives in silos

When payment data sits apart from customer data, you cannot see who buys what, how often, or when they stop. Marketing ends up guessing while finance works from estimates, and product teams fly blind. The insight that should drive decisions never forms because the raw material never meets.

How Integrated Payment Systems Reduce Business Costs

Nothing in this section depends on optimistic math. The savings come from deleting specific chores and specific losses, and most of them fall into four buckets.

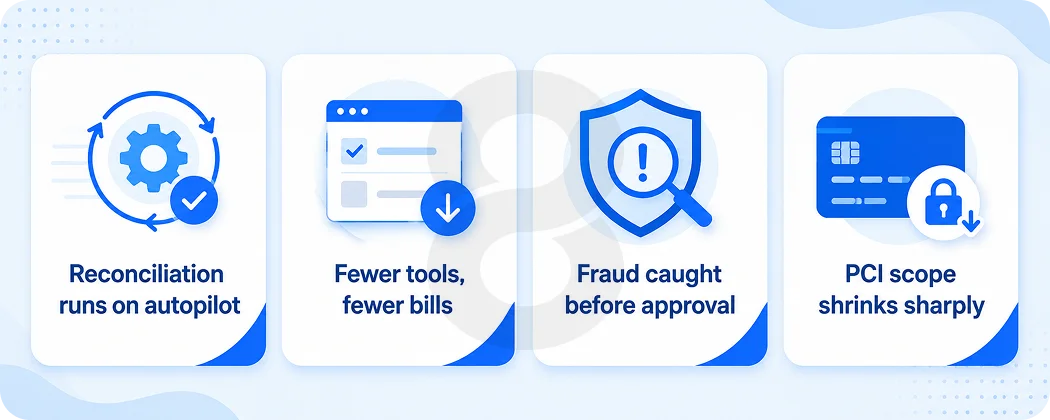

Automated reconciliation and accounting

Every settled transaction posts itself to the ledger, with sales, refunds, and fees sorted into the right accounts before anyone opens the books.

Month-end close stops eating days. The accountant who used to hunt discrepancies finally gets time to read the numbers and say something useful about them.

Lower processing overhead and fewer tools

A disconnected setup usually means four separate bills. One for the gateway, one for terminals, one for reporting software, one for reconciliation tools.

Integration folds those into fewer contracts, and pushing all your volume through one provider gives you real leverage when rate negotiations come around.

Reduced fraud and chargeback losses

Tokenization, encryption, and machine learning fraud screening now come standard on serious platforms, so suspicious transactions get caught before authorization instead of after the money leaves. Chargebacks fall too, because complete transaction records win disputes that vague ones lose.

Teams building AI-driven fraud detection into payment flows can go a step further and tune models to one specific business rather than leaning on generic rules.

Lighter PCI compliance burden

Card data that never touches your servers barely counts against your compliance scope. The provider shoulders the hard parts while your team fills out a short self-assessment instead of running a year-round security project.

It is worth pausing on how much money hides here. Full PCI compliance can demand network segmentation, quarterly scans, penetration testing, and audit fees, all of it recurring.

Handing that scope to a provider converts a permanent expense into someone else’s specialty. Small teams feel this most, because nobody hires a developer hoping they will spend half the year on compliance paperwork.

The side-by-side comparison makes the difference hard to argue with:

| Cost Area | Standalone Payments | Integrated Payments |

|---|---|---|

| Reconciliation | Manual, daily staff hours | Automatic, real time |

| Data entry errors | Frequent, found late | Rare, flagged instantly |

| Software costs | Multiple separate tools | One connected stack |

| PCI compliance | Full scope on your business | Mostly handled by provider |

| Chargeback handling | Manual evidence gathering | Automated records and alerts |

| Reporting | Stitched from exports | Single live dashboard |

How Integrated Payments Increase Sales and Revenue

Cost cutting gets attention. Revenue growth pays the bills. Integrated payments lift the top line in four measurable ways.

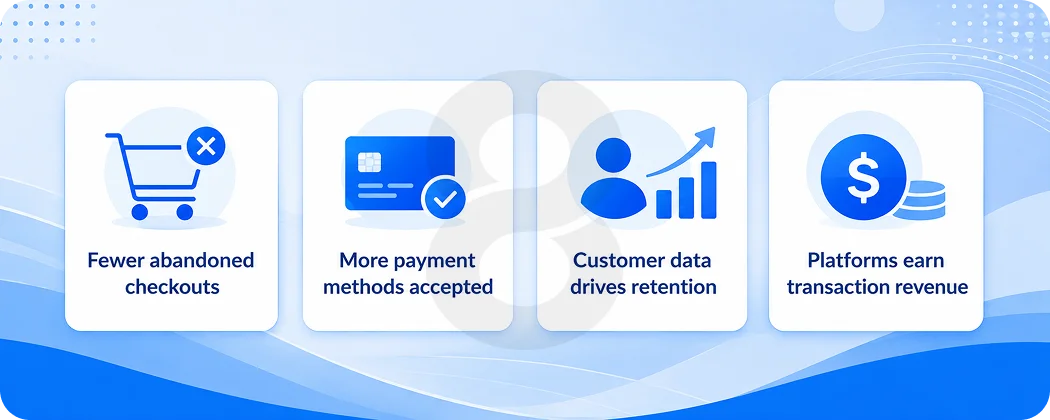

Fewer abandoned checkouts

Shoppers abandon roughly 70% of online carts. Long checkouts and forced redirects to external payment pages sit high on the list of reasons. Baymard’s research adds a detail worth sitting with. Around 13% of shoppers walk away when their preferred payment method is not on the list.

An integrated setup keeps the whole journey, from browsing to receipt, inside your own site or app. The flow has fewer steps and no redirects, which leaves fewer excuses to quit. Baymard estimates better checkout design alone could recover around $260 billion in lost orders across the US and EU. Even a small slice of that math changes a business.

More payment methods without more complexity

Customers expect choice between cards, digital wallets, bank transfers, and buy now pay later. Bolting each method onto a standalone system means separate integrations and separate headaches.

An integrated platform adds new methods through configuration, not months of development. Every added method captures sales that would have walked.

Customer data that actually sells

Once payment data and customer data live together, buying patterns stop being guesswork. The repurchase rates, the customers drifting toward churn, the price points that convert, all of it becomes visible.

That visibility feeds loyalty programs, sharper offers, and inventory decisions grounded in what people actually buy. A well-designed mobile app with embedded payments turns every purchase into a signal worth acting on.

Retention is where this pays off hardest. Keeping an existing customer costs a fraction of winning a new one, and payment data flags the fade before it becomes a loss. A subscriber’s card fails, or a weekly buyer goes quiet for a month, and the system notices.

Respond at that moment with the right nudge and you keep revenue that would have drained away without anyone spotting it.

New revenue streams for software platforms

SaaS companies and ISVs get to play a different game entirely. Embed payment processing into the product, and the platform earns a cut of every transaction its merchants run. As usage grows, so does the revenue, with no extra sales effort behind it.

Stickiness comes along free, since merchants think very hard before leaving software that handles their money without drama.

How to Choose an Integrated Payment System in 2026

No single system fits every business, and vendors rarely volunteer that. The needs of a coffee shop, a subscription app, and a two-sided marketplace barely overlap. Match the system to the business first and worry about brand names later.

| Business Type | What Matters Most | Key Features to Demand |

|---|---|---|

| Retail and restaurants | Speed at the counter | POS integration, contactless, tipping, inventory sync |

| Ecommerce | Checkout conversion | One-page checkout, wallets, saved cards, fraud screening |

| SaaS and subscriptions | Billing reliability | Recurring billing, dunning, card updater, proration |

| Marketplaces | Split payments | Multi-party payouts, onboarding, escrow, compliance |

| Service businesses | Invoicing and field payments | Payment links, mobile terminals, scheduling sync |

Questions to ask any payment provider

A short list separates serious providers from sales decks:

- What does the full cost look like?

- Which payment methods and currencies work today?

- Is the API documentation readable, and how long do typical integrations run?

- When a transaction fails, what happens, and how fast does support actually respond?

- Who owns the transaction data and how painful is exporting it?

- How much of the PCI scope, tokenization, and fraud tooling does the provider genuinely cover?

Plan the integration itself

The provider is half the decision. The build is the other half. A clean integration maps payment events to your workflows, handles edge cases like partial refunds, and gets tested against real failure scenarios before launch. Rushed integrations work fine until Black Friday. Then they don’t.

Checkout design deserves equal weight. The best processing rates mean nothing if the checkout flow confuses people. Every extra form field is a small tax on conversion.

Read More: Custom Online Payment Gateway Development: Features, Cost, and Compliance Guide

How to Implement Integrated Payments Without Downtime

Migration anxiety is rational. Payments sit in a category of their own, where one bad day of failed transactions costs more than a year of quiet inefficiency. A careful rollout strips out almost all of that risk though, and honestly the process is more boring than scary.

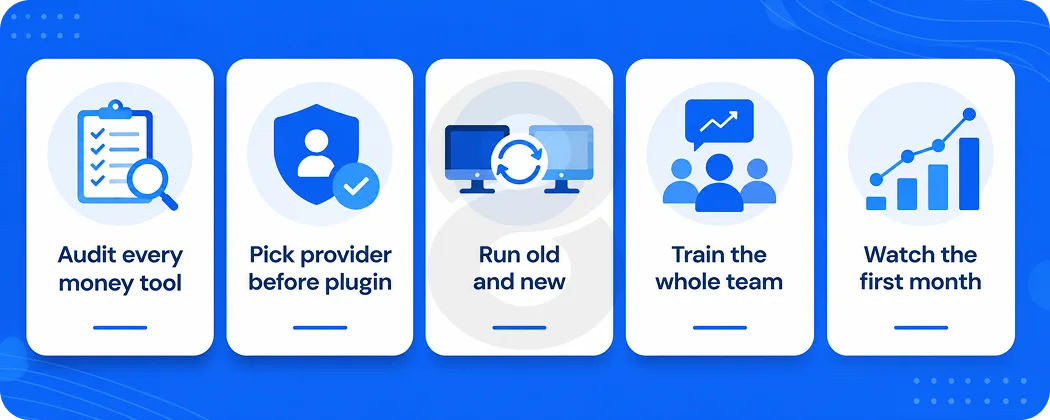

Audit what you run today

Before touching anything new, map what exists. Write down every tool that handles money, from the gateway and terminals through accounting, ecommerce, and invoicing. Then mark which ones exchange data automatically and which ones rely on a person walking numbers between them.

Most businesses discover far more manual handoffs than anyone admitted to. That map becomes the integration plan.

Pick the provider before the plugin

The provider decision comes first, and it rests on business model, pricing, and API quality. Only then does the connection question matter.

Prebuilt plugins cover the common platforms, while custom systems need real API work that deserves an honest line in the budget. A cheap provider with a miserable integration ends up costing more than a fair one with a clean build.

Run old and new in parallel

Flipping the switch overnight is how horror stories start. Route a slice of transactions through the new system while the old one keeps running, then compare settlement reports every day.

Pay attention to the weird cases, like partial refunds, failed captures, and currency rounding, because that is where integrations crack. Two clean weeks in parallel earns the confidence to migrate fully.

Train the people who touch it

Systems change faster than habits do. Finance needs to know where the reports moved, support has to learn the new refund flow, and whoever runs the counter deserves time with the new terminal before a customer is watching.

Skip this step and a perfectly good system starts generating support tickets. One hour of walkthroughs prevents weeks of confusion.

Watch the first month closely

The first thirty days tell you almost everything. Set alerts for failed payments, decline rates, and settlement mismatches, then treat every anomaly as urgent while it is still cheap to fix. Early catches also help because the team still remembers how the old process behaved and can compare against it.

Read More: Cost of Online Payment App: The Real Breakdown Nobody Gives You

Integrated Payment Trends to Watch in 2026

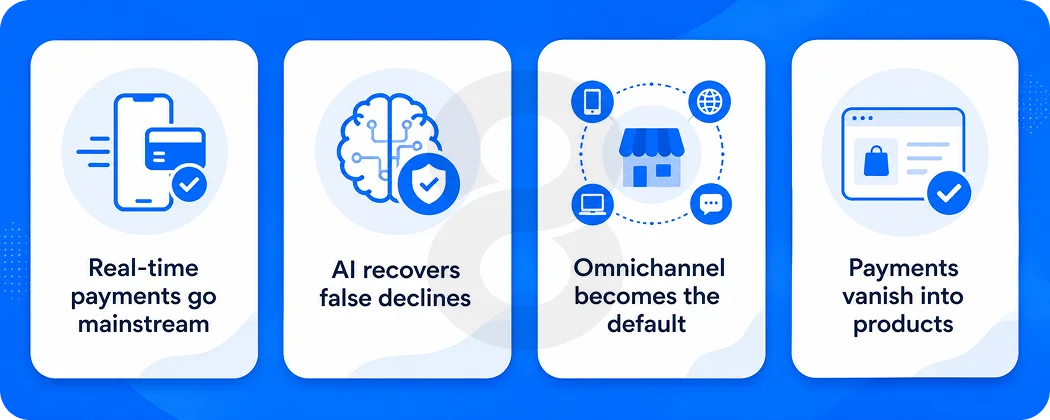

Three shifts matter for anyone building or buying payment systems this year.

Real-time payments go mainstream

Instant bank-to-bank rails like FedNow in the US keep expanding. Settlement in seconds instead of days changes cash flow for small businesses. It also pressures card economics, which is pushing processors to compete harder on value-added services.

AI moves from fraud blocking to revenue recovery

Fraud models used to answer one question. Is this transaction bad? In 2026, the better models also answer the opposite question. Is this good transaction about to be wrongly declined? False declines cost merchants more than fraud itself in many categories.

Omnichannel stops being optional

Customers no longer separate online from in-store. They browse on a phone, buy at a counter, and return by mail. They expect the business to treat all of that as one relationship. Unified commerce makes that possible by running every channel through one payment and data layer.

A purchase in the store shows up in the app, and saved cards work everywhere. Businesses still running separate systems per channel feel increasingly dated to their own customers.

Payments disappear into the product

Embedded finance keeps growing. Payments, lending, and payouts now live inside software people already use, from booking tools to accounting apps. Customers increasingly judge software by how invisible the payment step feels. The businesses winning in 2026 treat payments as part of the product experience, not a checkout formality.

How 8ration Builds Custom Integrated Payment Solutions

Buying a payment platform is easy. Making it work with your specific stack, workflows, and edge cases is where projects stall. That gap is where 8ration works.

The team has built integrated payment solutions across ecommerce stores, on-demand service apps, subscription platforms, and marketplaces. The work covers the full path. That means gateway and processor selection, API integration with existing POS and ERP systems, checkout and payment screen design, recurring billing logic, and fraud tooling tuned to the business.

For companies starting from scratch, 8ration builds web platforms and apps with payments designed in from day one, not bolted on later. For companies with existing systems, the team connects what you have to what you need without a risky rip-and-replace.

Every build ships with the unglamorous parts handled. Webhook reliability, idempotent retries, partial refund logic, settlement reporting, and PCI scope reduction. The parts nobody notices until they break.

Projects also start with numbers, not assumptions. The team measures current reconciliation hours, decline rates, and checkout drop-off before writing code. Those baselines make the return visible after launch. A payment system should prove its own value in the reports it generates.