Every founder who has ever paid a friend back on Venmo eventually has the same thought. How hard could it be to build one of these? The tap is instant and interface looks simple. Money just moves.

Then they actually start, and the floor drops out. Because the tap you see is the easy 5 percent. Underneath it sits fraud scoring, identity checks, ledger reconciliation, chargeback handling, and compliance stack that has to satisfy regulators in every country you touch. Building a wallet on PayPal’s level is less about the screen and more about the machine that makes the screen trustworthy.

This guide walks through what you are really signing up for. The features that matter, security you cannot skip, and an honest cost breakdown that does not pretend a payment app is the same as a to-do list.

Why Digital Wallets Became the Default Way People Pay

Look at the numbers and the appeal explains itself. Wallets used to be a convenience. Now they are how a large slice of the planet actually pays for things.

SQ Magazine puts digital wallet users past 5.2 billion in 2026, north of 60 percent of everyone alive. You are not slipping into a quiet corner of the market. You are walking straight into the middle of it.

PayPal is still the reference point everyone reaches for, and for good reason. It closed 2025 with 439 million active accounts and processed $1.79 trillion in total payment volume across the year.

When a client says they want digital wallet app development like PayPal, this is the scale they are picturing, even if their actual launch target is a single country and a few thousand users.

Here is the tired truth, though. The market being huge does not make your app inevitable. It makes it crowded. Apple Pay, Google Pay, Cash App, and Venmo already own the habit. So the real question is not whether wallets are a good business.

It is whether you have a wedge, a specific user or region or use case that the giants serve badly. Answer that before you write a line of code, and the rest of this gets a lot easier.

Core Features of a Digital Wallet App Like PayPal

Ask a founder what “like PayPal” means and they describe the surface. Send, receive, pay a merchant, done. But PayPal spent two decades stacking feature on top of feature, and trying to match all of it in version one is exactly how a build dies with nothing to show for it.

Think in tiers instead. What has to exist on launch day, what actually pulls users in, and what waits until you have traction and money to spend.

What users expect on day one

Miss any of these and the app reads as broken, not lean.

- Onboarding with KYC: Sign up, prove identity, clear the basic fraud checks. Your front door and your first compliance wall, in the same screen.

- Funding the wallet: A linked bank account or card so money flows both ways. Plaid and similar partners spare you the worst of this.

- Balance and history: Every dollar, every movement, visible. In a payment app, transparency is the product.

- Peer-to-peer transfers: The “sent you $20” moment that lands instantly. This is the feature that makes the whole thing feel alive.

- Alerts: Push notifications and fraud warnings, because users need to know the second money moves, especially when they were not the ones who moved it.

Read More: Custom Online Payment Gateway Development: Features, Cost, and Compliance Guide

The features that separate you from a toy app

Get the basics solid, and this next layer is what earns a permanent spot on someone’s home screen. QR and NFC payments make the app work at a real counter. Multi-currency support brings in cross-border users, and that is where a lot of the actual margin hides.

Then there is the stuff that pulls people back when they are not sending anyone money at all, bill pay, virtual cards, spending insights, rewards. Add an AI-assisted support layer and your support costs stop climbing in lockstep with your user count.

| Build Stage | What It Includes | Why It Matters |

|---|---|---|

| MVP (launch) | KYC onboarding, card and bank linking, balance view, P2P transfers, push alerts | Gets a real, secure product into users’ hands fast |

| Growth | QR and NFC payments, multi-currency, bill pay, virtual cards, spending insights | Turns a transfer tool into a daily-use wallet |

| Advanced | AI fraud scoring, rewards engine, crypto support, merchant tools, in-app support | Competes on retention and trust at scale |

Security and Compliance in Digital Wallet App Development

This is the part nobody wants to hear. Security is not a phase near the end of the timeline. It is the thing that decides your architecture on day one, and it is where most of your budget quietly goes.

A wallet holds two things people care about deeply. Their money and their identity. Lose either one, even once, and the app is finished. No amount of clean UI buys back that trust.

Compliance you deal with before you launch

Regulation is the wall every payment app hits, usually later than it should. In the United States you are looking at money transmitter rules that vary by state, plus federal reporting obligations.

Across markets you deal with KYC to confirm who your users are, AML monitoring to catch dirty money, and in Europe PSD2, which governs how payment data moves. None of this is glamorous. All of it is load-bearing.

The single most important standard is PCI DSS, the payment card industry rulebook for handling card data. Any wallet that touches card numbers has to meet it, and the requirements are published openly by the PCI Security Standards Council. Getting this wrong is not a bug you patch later. It is a reason your banking partners walk away.

How the money and data stay safe

Below the compliance layer is the protection that does the work. Encryption covers data both in transit and sitting at rest so a stolen database reads as gibberish to whoever grabbed it.

Tokenization goes a step further and replaces card numbers with useless stand-ins. Doing so keeps the sensitive stuff out of every place an attacker would think to look. Login gets locked behind biometrics and two-factor so a leaked password on its own opens nothing.

And fraud monitoring runs nonstop, because any static rule stops working the day a fraudster figures out what it is.

Machine learning is what makes that last part hold up. AI models that flag a fraudulent transaction as it happens catch the patterns a fixed rule set sleeps through, and they shift as the attacks shift. Past a certain size, you do not get to call this optional.

Technology Stack for a Scalable Digital Wallet App

This is where speed, security, and scale either hold together or come apart at the seams. No single stack is correct, but the winners tend to rhyme.

Up front, React Native or Flutter get you onto iOS and Android from one codebase, which counts for a lot when getting the app to feel identical on both platforms is half the fight in a payment product. Behind it, Node.js or a JVM setup like Spring Boot runs the payment flows, broken into microservices so one piece falling over does not drag everything down with it.

On the data side, PostgreSQL brings the transactional integrity a ledger cannot do without usually with Redis alongside it for caching and raw speed. Wrap the whole thing in AWS or Azure and you can go from a thousand users to a million without tearing it down and starting over.

And the software that moves money in the background, the settlement logic and reconciliation engine, is the least visible and most important part of the whole thing.

If your wallet is going to touch stablecoins or crypto, that is a separate build with its own rules. Blockchain rails for crypto support add real cost and real compliance weight, so decide early whether you actually need them or whether you are adding them because they sound impressive.

| Layer | Common Choice | What It Handles |

|---|---|---|

| Frontend | React Native, Flutter | Cross-platform mobile app |

| Backend | Node.js, Spring Boot | Payment logic, APIs, microservices |

| Database | PostgreSQL, Redis | Ledger integrity, caching, speed |

| Cloud and DevOps | AWS or Azure, Docker, Kubernetes | Scaling, deployment, uptime |

| Security | OAuth 2.0, 2FA, encryption, tokenization | Access control and data protection |

Cost to Build a Digital Wallet App Like PayPal

Here is the tab everybody actually opened. And the honest version is that anyone who fires back one number before asking you a dozen questions is just making it up.

Digital wallet app development like PayPal costs between $50K and $400K or more. That range is genuinely different products wearing the same name. A single-country wallet with core features and a small team lives near the floor. Stack on crypto support, multi-currency, AI fraud detection, and serious compliance, and you are near the ceiling, with room to push past $400,000 once ongoing security audits enter the picture.

Read More: Cost of Online Payment App in 2026: The Real Breakdown Nobody Gives You

The thing driving the price is almost never the feature count. It is how wide your compliance scope runs, how many payment integrations you are wiring up, and how much of the backend you build yourself versus rent. Here is roughly how those pieces stack up.

| Cost Driver | Relative Weight | Notes |

|---|---|---|

| Compliance and licensing | High | KYC, AML, PCI DSS, and money transmitter rules scale with every market you enter |

| Payment and banking integrations | High | Each gateway, bank API, and settlement partner adds build and testing time |

| Core feature development | Medium | Onboarding, transfers, and history are substantial but well-understood work |

| Security engineering | High | Encryption, tokenization, fraud systems, and audits are not where you cut corners |

| Backend and infrastructure | Medium to High | Real-time ledgers and scalable cloud setups cost more than a standard app backend |

| Maintenance and support | Ongoing | Budget 15 to 20 percent of the build cost per year for updates and security patches |

And one that blindsides teams on the regular. Launch day is not the end of spending. A payment app wants constant patching, monitoring, and compliance updates, and that annual bill is very real. Pencil it in now, or get surprised by it later.

How Long It Takes to Build a Digital Wallet App

You have seen the “wallet in 90 days” headlines. They are not lying to you, but read the fine print. Ninety days is real for an honest MVP, meaning secure onboarding, funding, and instant transfers, put together by a team that has done it before and leans on banking and payment partners instead of trying to rebuild the rails from scratch.

What blows the timeline is scope creep and compliance. Every extra country, every new payment method, every “can we just add crypto too” conversation pushes the date out.

A realistic picture looks like this. Three to four months for a focused MVP. Six to twelve months for a fuller wallet with contactless payments, multi-currency, and a proper fraud system. Longer if you are building for a heavily regulated market or handling licensing yourself.

The teams that hit their dates are the ones who said no to features early and shipped the boring, safe version first. The ones that slip are chasing PayPal’s entire twenty-year roadmap in their first release.

Testing is the other place timelines quietly disappear. A payment app cannot ship with the “we will fix it in production” mindset that works for a content app.

Automated testing and real-time monitoring have to be baked in from the start, because a bug in a wallet is not a broken button. It is someone’s money, and that is the kind of mistake users do not forgive or come back from.

Read More: Digital Wallet Solutions: Complete Guide for Startups in 2026

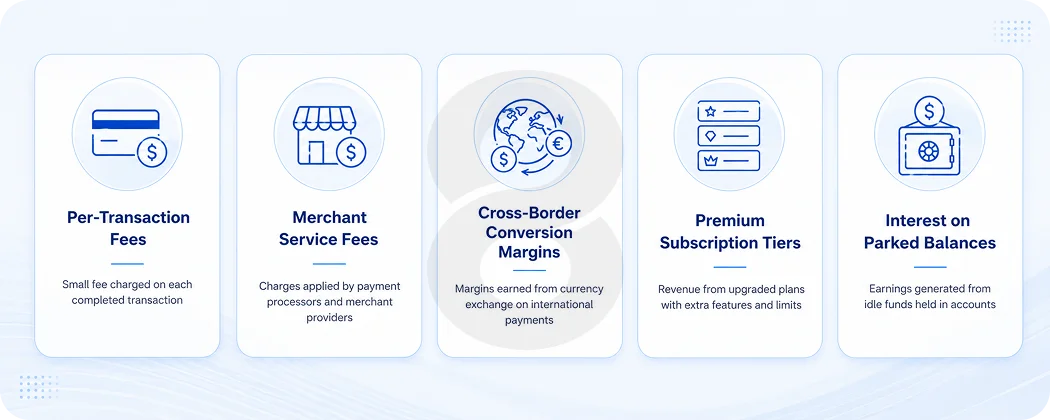

How Digital Wallet Apps Make Money

Say it out loud, because plenty of founders finish the app before they work out how it ever pays for itself. Running a wallet is expensive. Fraud losses, compliance, infrastructure, none of them stop sending invoices. So the revenue model cannot be something you circle back to.

The usual streams go like this. Transaction fees take a thin slice of each payment, and smart wallets charge the merchant rather than the sender so people keep sending without thinking about it. Merchant service fees work more like the card networks, where businesses pay for the privilege of accepting wallet payments.

Cross-border and currency conversion quietly turns into one of the fattest margins you have once international users show up. Premium tiers sell faster transfers, higher limits, and better analytics. And the balances people leave parked in the wallet earn interest while they sit there.

The wallets that make it rarely bet on one stream. They run a few at once and let the balance shift as they grow. The real move is choosing early, because how you charge decides who shows up and what you build next.

A wallet made for cheap P2P transfers has almost nothing in common with one made for cross-border merchant payments, even though both get pitched as building something like PayPal.

Read More: Top Banking Software Solutions to Modernize Your Financial Services in 2026

Build Your Digital Wallet App With 8ration

Plenty of agencies can build an app. Far fewer have shipped something that moves real money and survives a regulator’s questions. That gap is where most wallet projects quietly fall apart.

8ration treats digital wallet app development like PayPal for what it is. Compliance and security get scoped at the start so KYC, AML, and PCI DSS shape the architecture instead of ambushing it three weeks before launch. Payment integrations, ledger design, and fraud monitoring get built as core engineering, not patched in once someone notices they are missing.

The edge is working with people who live inside fintech products all day instead of treating your wallet as their first rodeo. Run from discovery through deployment and into post-launch monitoring, the process is set up to catch the pricey mistakes while they are still cheap.

What you get out of it is a leaner MVP that ships on schedule, security layer that actually holds, and clear path to add contactless payments, multi-currency, or crypto once real users are telling you which one they want.

Weighing a PayPal-scale wallet against a smaller regional play or a single sharp feature? That is the conversation to have before anyone writes code. Scoping it right early saves more than any framework decision ever could.

Read More: 30 Best Cryptocurrency Wallet Apps for 2026