Fintech apps do not fail because the interface looks dated. They fail for boring reasons. A skipped KYC step. Card data sitting in a database it had no business being in. Security duct-taped on during the last sprint before launch.

Meanwhile the money keeps growing, with the global fintech market on track for $460 billion in 2026 and digital payment volume expected to blow past $26 trillion this year. That much money moving through apps has made financial software the single favorite target of cybercriminals worldwide.

Fintech app development is the process of building software that moves, stores, lends, or manages money. Payments, digital wallets, neobanks, lending platforms, trading apps, insurance tools… every one of them handles the two things people trust least to strangers: their money and their identity. Get that trust wrong once and there is no second launch.

Read More: Digital Wallet App Development Like PayPal: Cost, Features, Security

This guide walks through what building a secure financial app takes in 2026. The regulations you cannot dodge, architecture decisions that decide whether you pass a bank’s due diligence, realistic costs, and where teams burn money for nothing.

Why Fintech App Development is Harder Than Regular App Projects

A food delivery app going down for an hour annoys people. However, payments app with one exposed API endpoint drains accounts. That difference shapes every decision in fintech app development, from your database schema to your onboarding screens.

Three groups are watching you the moment you go live. Regulators like the SEC, CFTC, and state financial authorities. Payment networks like Visa and Mastercard, who can cut you off faster than any government agency.

And users, who are more privacy-aware in 2026 than they have ever been, and who will read your app store reviews before trusting you with a bank connection.

Then there are the attackers, who had a very good year. In the World Economic Forum’s latest Global Cybersecurity Outlook, 77% of business leaders reported a rise in cyber-enabled fraud and phishing, and 73% said fraud touched them or someone in their network last year.

What used to take a skilled criminal a week now takes an AI a minute. The old goal was preventing a breach. The realistic goal now is surviving one, and your threat model should be written accordingly.

That is also why fintech projects lean on experienced teams. A generalist shop that has shipped twenty e-commerce apps has never dealt with a money transmission license or a PCI audit. Partnering with people who build custom software for regulated industries changes the conversation from “can we ship this” to “can this survive an audit.”

Fintech Compliance Requirements in 2026

Compliance in fintech is not one certification. It is a stack of overlapping obligations that shifts depending on what your app does and where your users live. Here is the map for 2026.

PCI DSS 4.0

Touch card data anywhere in your flow and PCI DSS owns you. Yes, even if a processor tokenizes the card number before you ever see it. The 4.0 version has been mandatory since March 2025, and it raised the bar on targeted risk analysis, MFA, and payment page scripts.

Fall out of compliance and the fines can run past $100,000 a month. Worse, the card networks can simply cut you off, and at that point the fine is the least of your problems.

The smart move is scope reduction. Use tokenization and hosted payment fields so card data never enters your systems. A smaller cardholder data environment means fewer systems in audit scope, which cuts certification cost dramatically.

Read More: Custom Online Payment Gateway Development: Features, Cost, and Compliance Guide

KYC and AML

Regulators assume that if your app can move money, criminals will try to move dirty money through it. Know Your Customer and Anti-Money Laundering rules are how they make that your problem. The 2026 expectations are heavier than they were even two years ago. And it never ends. This is a permanent operating cost, not a launch task.

Which is why almost nobody builds identity verification themselves anymore. Plugging in Onfido, Jumio, or Persona hands the hardest part to a specialist and leaves you with a clean compliance trail to show auditors.

Regional Data Laws

Where your users live decides which privacy regime you answer to. Serve anyone in the EU and GDPR applies, full stop. American users bring CCPA plus whichever state privacy laws have passed since you last checked, because the list keeps growing.

European payments carry PSD2’s Strong Customer Authentication rules, and PSD3 is rolling out through 2026 and 2027 to stretch open banking into open finance. The US finally federalized its own piece of this too. Open banking API access now falls under CFPB Section 1033.

Read More: Top Banking Software Solutions to Modernize Your Financial Services in 2026

Licensing

If your app holds customer funds or moves money between users, you likely need a Money Transmission License in every US state where you operate.

No federal license exists to shortcut this. Each state takes 3 to 6 months, so startups that want to launch this year usually rent someone else’s license instead. Partnering with an already-licensed provider turns a 12-to-18-month slog into 6 to 9 months.

Regulators have a name for where all of this is heading… compliance-by-design. Compliance logic now lives in the codebase. API gateways that validate KYC status before any data moves. Retention policies enforced at the infrastructure level instead of documented in a PDF nobody reads.

Read More: Integrated Payment Solutions: How Businesses Cut Costs and Boost Revenue in 2026

How to Build a Secure Fintech App Architecture

Security in a financial app is not a feature list. It is a layered defense where every layer assumes the one before it has already failed. Here is what that looks like in practice for fintech app development in 2026.

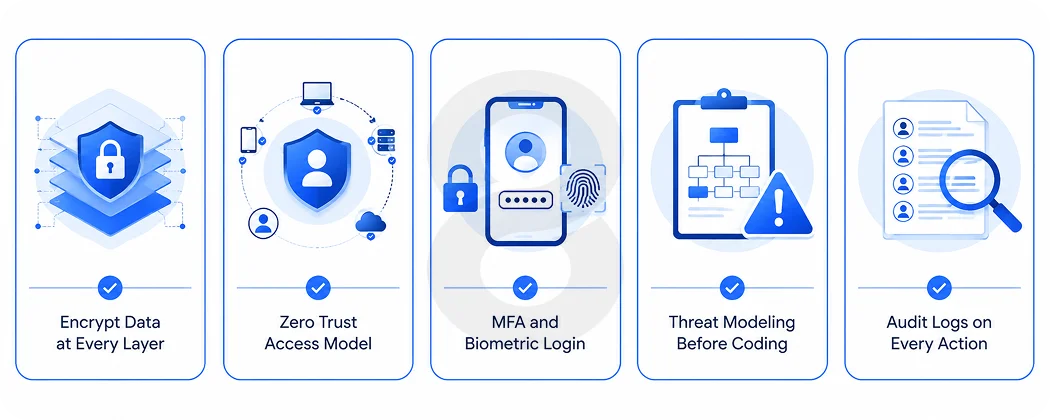

Encryption everywhere

AES-256 at rest, TLS 1.2 or newer in transit (push for 1.3 where your stack supports it). And encrypt the sensitive fields inside the database itself. Disk-level encryption protects you from someone stealing your hardware, not from someone stealing your queries.

Zero trust as the default

The perimeter model assumed everything inside your network could be trusted. That assumption died the moment users started logging in from airport WiFi. So trust nothing. Authenticate every API call. Log every action. Authorize every query by role. When credentials look compromised, kill the access first and investigate second.

Authentication that actually holds

Verizon’s Data Breach Investigations Report found that 88% of basic web application attacks involved stolen credentials. Read that again, because it means most attackers walk in through the front door. Biometric login, device binding, and MFA are the floor now.

Higher-risk products are going further with continuous behavioral authentication, where the system quietly watches typing rhythm and usage patterns and flags anything that stops looking like you.

Threat modeling before architecture

Run STRIDE analysis early. It changes real decisions, like keeping auth tokens out of app memory and in secure device storage instead.

Read More: AI in Banking: How Intelligent Systems Are Transforming Financial Decisions

Audit logging on everything

Every action tied to an authenticated identity, logged, and retained. Banks will ask for this during due diligence, and regulators will ask for it during investigations.

One thing worth saying plainly: security that frustrates users costs you as much as security that fails. If your MFA flow takes ninety seconds, people abandon the app. The craft is making the security invisible where risk is low and firm where risk is high.

Half of that balance gets decided in interface decisions. Put your designers and your security people in the same room from sprint one, or watch them undo each other’s work for a year.

Must Have Features for Financial Apps in 2026

The baseline has moved. Five years ago, a clean dashboard and push notifications felt modern. Now users expect their financial app to think ahead of them.

Core features every financial app needs

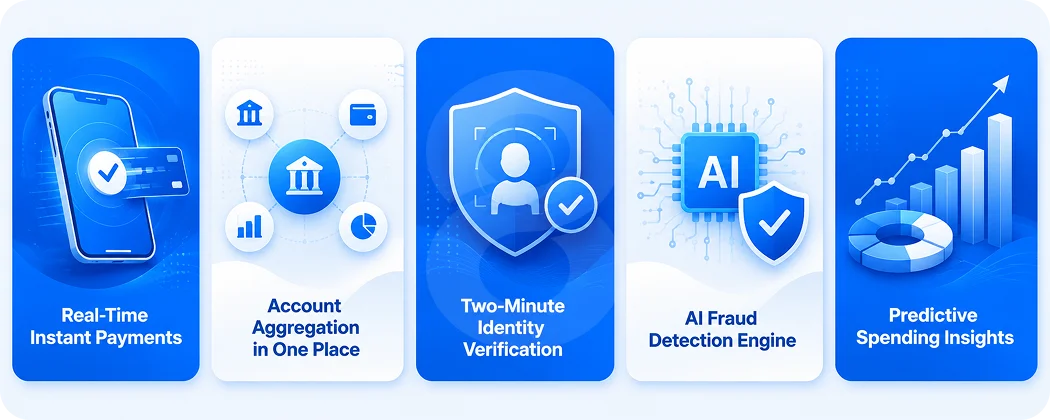

- Account aggregation, so users see all their money in one place. Open banking APIs handle the plumbing, with OAuth 2.0 and OpenID Connect doing the securing.

- Real-time payments. FedNow volume grew 460% in 2025 and moved $853.4 billion, and users now treat instant settlement as normal. Three-day transfers feel broken.

- Instant identity verification during onboarding, ideally under two minutes end to end

- Biometric login with device binding

- In-app support and dispute handling

- Spending insights and categorization

What separates leaders from the pack

- Predictive nudges. A message like “you’re on track to hit your savings goal 12 days early” does more for retention than any static balance screen ever will.

- LLM assistants, built the way modern AI chatbots are, that can actually answer “why was I charged this” in plain language instead of dumping a transaction code on the user

- Personalization the user controls. Show people what data drives their experience and let them switch it off. The line in 2026 sits between helpful and creepy, and users who feel watched rather than helped delete the app and never look back.

Behind all of this, AI carries the heaviest load where nobody sees it: fraud. Real-time fraud detection is the most battle-tested AI use case in the industry. A serious system stacks three things together.

Supervised models trained on known fraud, anomaly detection for the patterns nobody has labeled yet, and graph networks that catch organized rings a single-transaction view would miss. The engineering challenge is speed.

Fraud scoring has to happen inside the payment authorization window, in a few hundred milliseconds at most, or declines and friction pile up that users blame on you, not the fraudster. Building this kind of intelligent decisioning layer is where most fintech products now sink their most serious engineering effort.

He is pointing at ECOA and fair lending rules, which effectively force explainable AI techniques like SHAP values or inherently interpretable models for any credit decisioning. Plan for that from the start, because swapping model architectures after launch is a rebuild, not a patch.

Read More: 15 Fintech Industry Trends for Innovative App Development 2026

Best Tech Stack for Fintech App Development

There is no single correct stack, but there are patterns that keep showing up in fintech products that scale without falling over.

Mobile

Flutter or React Native for cross-platform speed, Kotlin and Swift when native performance and platform-level security APIs matter more. Most consumer fintech starts cross-platform and goes native for specific high-security modules.

If mobile is your primary channel, and for consumer fintech it almost always is, getting the mobile build right decides your app store ratings, and your app store ratings decide your acquisition cost.

Backend

Microservices over monoliths for anything expecting real transaction volume. Payments, auth, ledger, and notifications each scale independently, and a spike in one does not take down the rest. Node.js, Java, and Go dominate. Event-driven architecture handles transaction streams without the database becoming the bottleneck.

Infrastructure

AWS or GCP, configured against their compliance-certified baselines rather than defaults. Define everything as code, because an environment you can rebuild from a repo is an environment you can prove things about during an audit.

Then wall off the payment systems from everything else through network segmentation. The bonus nobody mentions: that same segmentation shrinks your PCI scope, which shrinks your audit bill.

Integrations

Plaid or similar for bank connections, Stripe or Adyen for processing, a dedicated KYC provider, and a real-time fraud engine. Buying these instead of building them is almost always right in year one, though stitching them together cleanly is its own discipline of system integration work.

Web still matters more than founders expect. Admin dashboards, business-facing portals, and the marketing site that has to convert skeptical users all run through a web platform that shares the same security posture as the app itself. Attackers do not care which surface they get in through.

Read More: List of Best Mobile Banking Apps to Inspire Your Fintech Solution

How Much Does It Cost to Build a Fintech App in 2026

The honest ranges, without the sales gloss. $50K to $150K buys a focused fintech MVP. Add lending or investment features and you land somewhere between $150K and $350K. A production-ready neobank or crypto banking product starts around $350K and climbs past $600K without much effort.

Now the part that catches founders off guard. Compliance and security swallow 25 to 40 percent of whatever total you land on. That is not padding. It is encryption, audit logging, penetration testing, KYC integration, and the documentation trail regulators and bank partners demand.

Timeline follows the same logic. A basic MVP takes 4 to 8 months. A full-scale platform takes 9 to 18 months, and state licensing can add months on top if you are going the direct route rather than partnering with a licensed provider.

One more number worth burning into memory. Pre-build regulatory strategy work costs $80,000. A mid-development compliance rebuild costs 2 million. Industry estimates put reactive compliance at 5 to 20 times the cost of building it in from the start.

Read More: Fintech App Development Cost in 2026: Full Breakdown by Feature, Team & Region

Nobody plans to be the second case. Plenty of teams end up there anyway because they treated compliance as a launch-week task.

Common Fintech App Development Mistakes to Avoid

Watching fintech projects go sideways is educational. The failure modes repeat.

Storing card data directly

The most expensive rookie mistake in the category. Tokenize through your processor and keep card data out of your systems entirely. Your PCI scope shrinks, your liability shrinks, your audits get cheaper.

Treating compliance as a final review

Compliance added at month eight means rearchitecting databases and rewriting APIs at month nine. Rules change too, so your architecture has to absorb regulatory updates without a full rewrite.

Underestimating bank due diligence

Sooner or later, almost every fintech app needs a bank partner. And here is what founders learn the hard way: banks do not care how good your pitch deck is. They care whether you look like an organization that can handle their money.

Can you show a change management process? An incident response plan that has been tested? Audit trails going back to day one? That posture takes months to build, so start building it in month one. Trying to manufacture it during fundraising is how deals die.

Ignoring the ledger

Money math has to be exact, idempotent, and reconcilable. Teams that treat the ledger as a regular database table discover during their first reconciliation cycle why double-entry accounting has survived five centuries.

Manual compliance processes

Manual KYC reviews and manual monitoring do not scale past a few thousand users. Automate early or drown in ops cost.

Frankenstein teams

Splitting the frontend, backend, and integrations across disconnected freelancers creates seams, and seams in fintech are vulnerabilities. A coordinated full stack team that owns the product end to end closes the gaps that piecemeal delivery leaves open.

Read More: Custom Accounting Software Development: Why Businesses Invest in It

How to Start Fintech App Development: Step by Step

The order matters. Start with features and deal with regulation later and there is a good chance you will build part of the product twice.

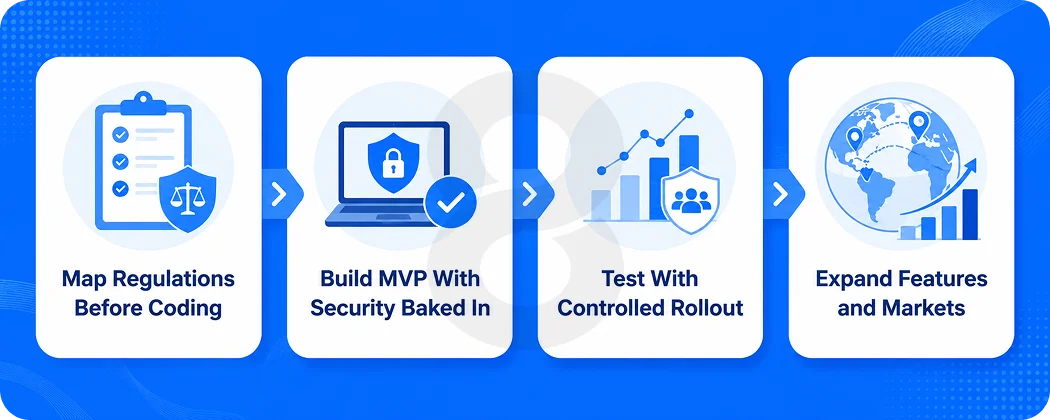

Step 1: Find out which rules apply

Before anyone writes code, define what the app actually does. Does it hold money or only display financial data? Where will it operate and which users will it serve? Those details decide the regulatory path.

A budgeting app that reads bank data has a much lighter burden than a wallet that holds customer funds. A lending product has to deal with credit rules that do not apply to a payment app.

Answer these questions before development starts:

- Will the app hold or transfer customer money?

- Will card data touch your systems?

- Will the product approve loans or make credit decisions?

- Which countries or US states will it operate in?

- Will you work through a bank, processor, or licensed fintech provider?

The answers affect the architecture, integrations, budget, and launch date. Leave them unanswered and the uncertainty gets priced into the project later.

Read More: How to Build an Online Payment App: Features, Architecture, and Development Process

Step 2: Build one core flow properly

The first version does not need every idea from the roadmap. It needs one financial flow that works from beginning to end.

That might be opening an account, connecting a bank, sending money, or applying for credit. Whatever the flow is, it still needs proper authentication, encryption, permissions, and audit logs. An MVP can have fewer features. It cannot have weaker security.

Build OAuth, tokenization, access controls, and logging into the foundation. Trying to add them once the app is nearly finished often means changing databases, APIs, and onboarding screens that the team thought were done.

Step 3: Test it with a limited group

Do not wait for a public launch to discover that identity checks take too long or that the fraud system blocks real customers.

Start with a controlled user group or a smaller market. Track where people leave the onboarding process, how often verification fails, which transactions trigger false alerts, and how long support takes to resolve a dispute.

Test the operation behind the app too. Reconciliation, monitoring, incident response, and customer support all need to work before volume increases.

A social app can recover from a rough beta. A fintech app may not recover from a missing payment or a locked account.

Read More: Average Timeline and Budget for a FinTech App with Real-Time AI Fraud Detection

Step 4: Expand after the main flow works

Once users can complete the main task reliably, add more features, markets, integrations, and licenses.

Let usage data guide the order. Customers may care more about faster transfers than investment tools. They may need better spending controls before another account type.

Each new market can bring different privacy, reporting, identity, and licensing rules. Check those before the feature enters development.

This is where the work done in the first two steps starts paying off. A product built around clear permissions and traceable transactions is much easier to expand than one held together by fixes added before launch.

To develop fintech software in 2026 means accepting regulation as part of the product. Teams that do this early are more likely to pass audits and secure bank partnerships. Teams that avoid it usually spend their runway correcting decisions they made months earlier.

How 8ration helps with fintech app development

8ration does not treat a fintech app as a standard mobile build with a payment screen added to it. The work starts with the parts that can derail the project later.

From there, 8ration can handle the mobile app, web platform, backend, APIs, payment connections, KYC tools, fraud systems, and internal dashboards. The same team can also set up authentication, permissions, transaction logs, testing, deployment, and ongoing maintenance. That shared ownership matters more than it sounds.

When separate freelancers build the frontend, backend, and integrations, problems tend to land in the space between them. While payment processor says the app sent the wrong request, mobile developer blames the API. The backend developer says the requirements changed. Meanwhile, the transaction is still broken.

Read More: How to Hire Fintech Developers: Complete Guide for Startups and Enterprises

8ration keeps those systems under one technical plan. The app, backend, integrations, and internal tools are designed to work together, which makes transactions easier to trace and incidents easier to investigate.

The team also helps founders avoid building things they should be buying. KYC verification, card tokenization, payment processing, and bank connectivity usually belong with specialist providers, especially in the first release. Custom development should go toward the part that makes the product worth using.

For a payment app, wallet, lending platform, investment product, or a larger fintech system, 8ration can take the project through scoping, development, integration, testing, and launch without splitting responsibility across several disconnected teams.

Read More: Digital Wallet Solutions: Complete Guide for Startups in 2026